1. The Next Evolution in Lending Intelligence

For years, banks and NBFCs have relied on credit scoring engines and loan management systems to make lending decisions.

But the lending landscape is shifting – faster, more digital, and data-heavy.

Credit scores still matter, but they often don’t reveal the complete borrower story. A 780 score might look perfect, but what if that person’s recent bank statement shows frequent overdrafts, salary delays, or high daily expenses? That’s where bank statement insights are becoming the next big differentiator in lending intelligence.

A recent report by Deloitte revealed that over 62% of lending decisions now include cash flow data derived directly from bank statements – because it paints a live picture of borrower behaviour that static credit scores can’t.

2. Why Bank Statement Insights Matter More Than Ever

Bank statement insights go beyond numbers – they interpret borrower intent.

They show how people spend, when they repay, and how stable their income patterns are.

For lenders, this means:

- Improved decision accuracy – evaluating real repayment capacity.

- Faster risk identification – spotting warning signals early.

- Proactive collections – predicting defaults before they happen.

Your loan management system becomes smarter when it’s fuelled by these insights – not just credit history, but live financial behaviour.

If you’ve already explored our Ultimate Bank Statement Analyser Guide, you’ll know how deep data parsing works to extract meaning from months of raw transactions – helping lenders see beyond a borrower’s CIBIL score.

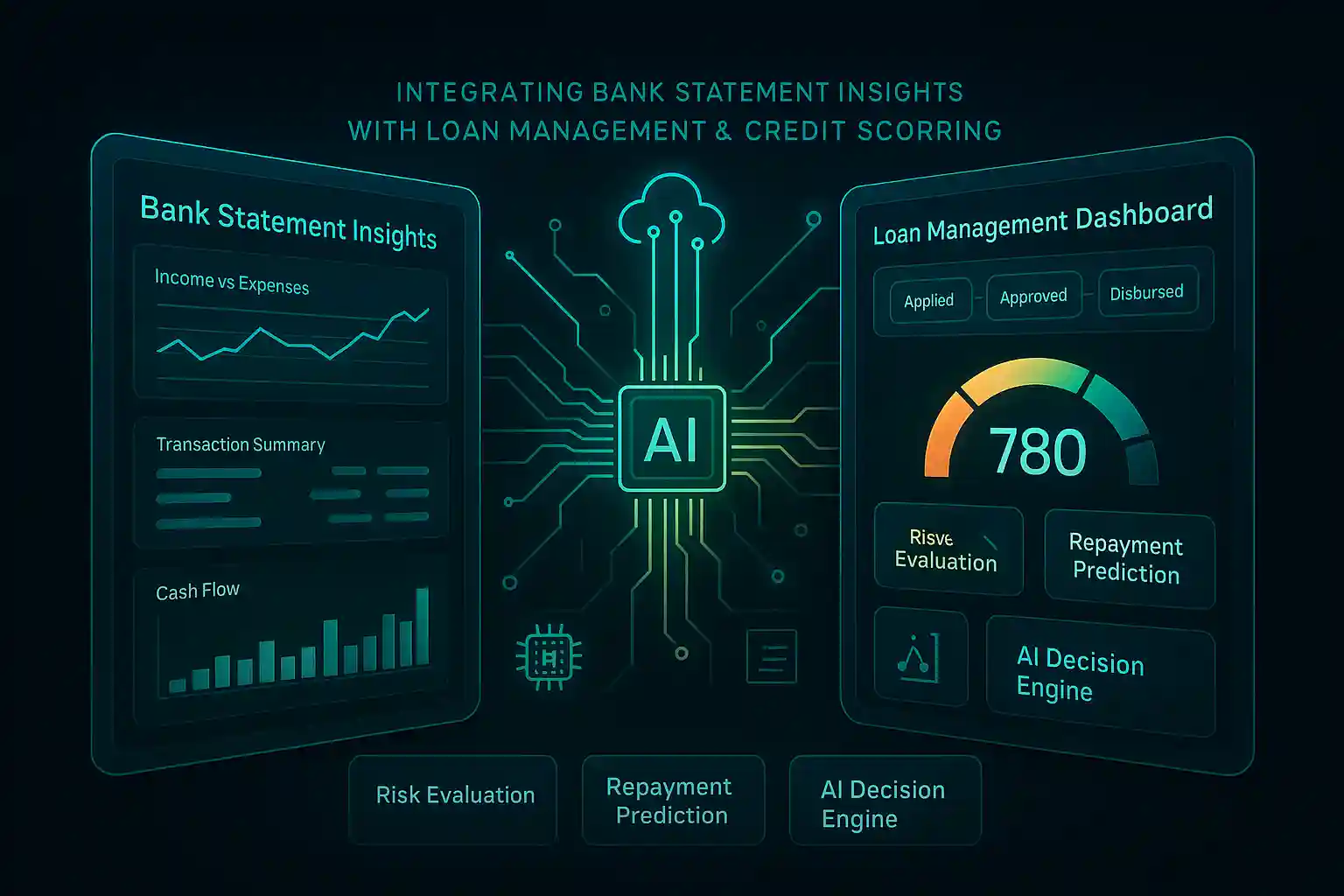

3. The Integration Advantage: Loan Management Meets Data Intelligence

Integrating bank statement insights directly with loan management systems creates a real-time loop between credit assessment, approval, and recovery.

Here’s what this integration changes for lenders:

a. Faster & Smarter Approvals

Loan officers get instantly analyzed financial patterns alongside credit scores – no manual data crunching.

Example: If an applicant shows stable income inflows for 12 consecutive months with low EMI obligations, the system can auto-flag them as low-risk.

b. Better Risk Scoring Models

Integrating statement insights helps credit scoring engines adjust their algorithms dynamically.

It means lenders can re-score borrowers monthly, based on ongoing financial health, not just historic bureau data.

c. Proactive Default Prevention

Data shows that borrowers with more than three consecutive months of declining income have a 45% higher chance of missing EMIs.

Integrated systems can detect these changes early, triggering alerts for the collections team.

d. Seamless Collections Workflow

Collections teams can use insight-driven segmentation – reaching out differently to borrowers flagged for “temporary liquidity issues” versus “chronic over-expenditure.”

These are not just features; they’re the new backbone of data-driven lending.

4. From Insights to Action: How Integration Works in Practice

When a lender integrates their loan management platform with an analyser through a bank statement analysis API, here’s the chain reaction:

- Borrower uploads their statement.

- The bank statement analyser extracts and classifies transactions.

- Bank statement analysis software scores income stability, expenses, and repayment patterns.

- Data flows automatically into the loan management dashboard.

- The system calculates risk tiers or adjusts loan limits dynamically.

This kind of integration cuts manual review time by up to 70%, based on fintech benchmarks published by PwC India.

If you’ve read our blog Loan Approval Workflow: From Application to Decision, you’ll notice this integration fits right into that pipeline – streamlining every stage between application and disbursement.

5. How AI Enhances the Integration

Artificial Intelligence makes this process more predictive.

By recognizing thousands of transaction patterns, AI can classify borrower types – steady salaried, volatile self-employed, or high-spend lifestyle customers – and recommend lending strategies.

As highlighted in How AI Is Changing the Way Lenders Use Bank Statements for Loan, automation isn’t just about speed; it’s about precision.

AI helps lenders focus on intent, not just information.

6. Expert Insights: Industry Voices

“The true credit risk is hidden between the lines of a bank statement. Integrating that insight into loan management is where the future lies.”

— Suresh Naidu, Chief Risk Officer, NBFC India

“Credit scoring models become 35–40% more accurate when paired with live statement data.”

— FinTech Association of India Report, 2024

“The combination of transactional analytics and credit history gives lenders a 360° borrower profile — it’s smarter, safer, and faster.”

— Ritika Bansal, Senior Lending Consultant, Axis Digital Finance

7. Detecting Red Flags Before Defaults

Integration also enhances early warning systems.

For instance, our earlier post — 5 Red Flags to Watch for in Bank Statements Before Approving a Loan – discusses recurring negative balances, sudden cash inflows, or delayed salaries.

When connected to a loan management system, these red flags can automatically trigger preventive actions – like pausing disbursals or reviewing repayment schedules.

That’s how proactive collection becomes possible – before a borrower ever misses an EMI.

8. Building a Data-Driven Lending Ecosystem

Integrating statement insights with loan management and credit scoring isn’t about replacing old systems – it’s about enhancing them.

Lenders gain:

- Rich borrower profiling

- Quicker approvals with reduced manual review

- Early detection of financial stress

- Stronger collection efficiency

And for growing fintechs, this is the bridge between traditional risk models and intelligent automation.

9. Wrapping It Up

As the lending industry evolves, the smartest players will be those who can connect insights to action.

That’s exactly what integrating bank statement insights into loan management systems achieves – smarter credit scoring, faster decisions, and fewer defaults.

If you’re exploring how to bring these insights into your ecosystem, our ProAnalyser platform provides the foundation – with APIs ready for integration, advanced analytics, and AI-driven accuracy that lenders trust.