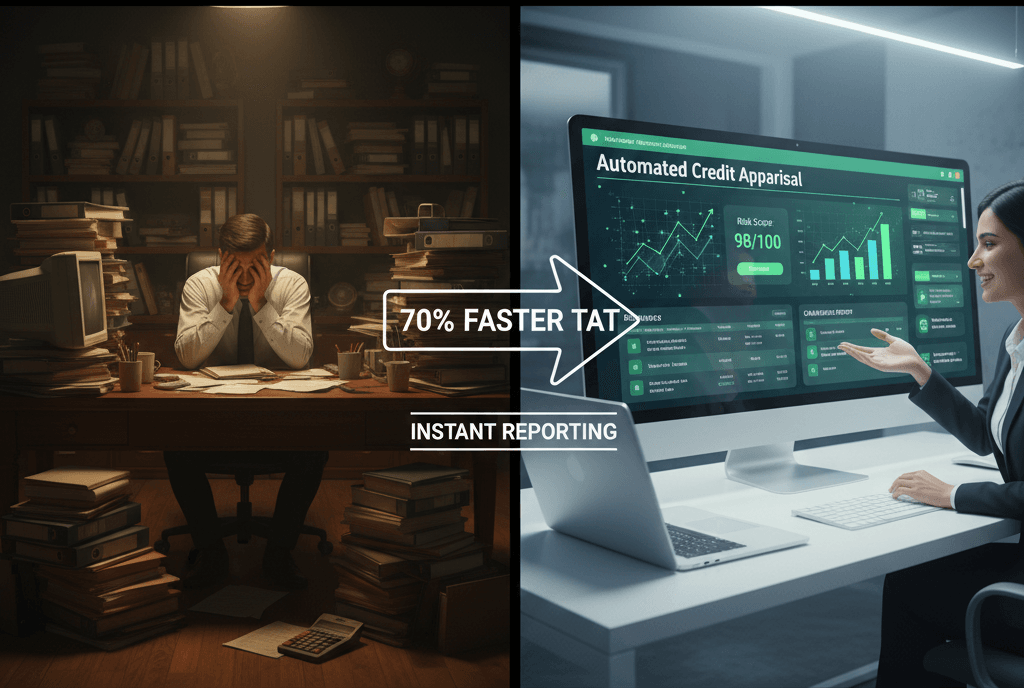

In the competitive world of lending, speed isn’t just an advantage – it’s a survival requirement. Today’s borrowers, from retail individuals to seasoned MSME entrepreneurs, value time as much as interest rates. If your Loan Turnaround Time (TAT) is measured in weeks while your competitor’s is measured in hours, you aren’t just slow; you’re losing business.

The bottleneck is almost always the same: the manual credit appraisal process. However, a shift is happening. By leveraging automated credit appraisal, forward-thinking institutions are transforming their back-office from a slow-moving hurdle into a high-speed engine for growth.

Why Manual Credit Appraisal is the Bottleneck of Modern Lending

Traditional credit underwriting is a labor-intensive craft. For decades, credit officers have spent the bulk of their day “punching data.”

The Drain of Manual Data Entry and Financial Spreading

The most significant time-sink in any credit department is financial spreading. Manually migrating data from scanned PDFs, tax audits, and balance sheets into Excel is slow and prone to fatigue errors. According to Investopedia, underwriting requires a meticulous assessment of risk, but when your best analytical minds spend 60% of their time on data entry, your operational efficiency plateaus.

Human Bias and Error in Ratio Analysis

Manual analysis is subjective. One credit manager might be conservative with a DSCR calculation, while another is more liberal. This inconsistency leads to erratic decision making. Furthermore, when rushing to meet deadlines, it is easy to miss subtle early warning signals (EWS) buried deep in the notes to accounts.

Explore Further: If you want to see how technology is reshaping this landscape, check out our blog on how credit appraisal is being reinvented with smart data analytics.

4 Ways Automated Credit Appraisal Slashes Loan TAT

Transitioning to a digital underwriting engine like Pro Analyser doesn’t just make the process faster—it makes it smarter. Here is how automation changes the game:

1. Instant Bank Statement and GST Analysis

Evaluating a borrower’s cash flow shouldn’t take days. A modern Bank Statement Analyser can process hundreds of pages of transactions in seconds. It instantly flags circular trading, bounced checks, and irregular cash withdrawals—giving you a risk profile before you’ve even finished your coffee.

👉 Simplify your document review and get started with our Bank Statement Analyzer to accelerate your approvals today.

2. Rapid CMA Report Generation

For corporate lending, the CMA report is the gold standard. Generating these manually is a nightmare of formulas and cell-linking. Automated credit appraisal tools can generate a complete, bank-ready CMA report in minutes, pulling directly from the audited financials.

3. Automated Ratio Analysis and Scoring

Automation allows for instant, standardized ratio analysis. Whether it’s the Current Ratio, Debt-to-Equity, or complex Cash Flow Analytics, the system calculates them with 100% accuracy. This allows the credit officer to spend their time interpreting the data rather than calculating it.

Deep Dive: To master this process, read our comprehensive guide on how to conduct a credit assessment using bank statements.

Beyond Speed: Enhancing Quality with Digital Underwriting

Lenders often fear that speed kills quality. In reality, automated credit appraisal enhances risk mitigation and ensures alignment with RBI regulatory frameworks regarding credit discipline.

- Fraud Detection: Algorithms can detect “window-dressed” balance sheets or manipulated PDFs that are invisible to the naked eye.

- Probability of Default (PD): Machine learning models can compare a borrower’s profile against historical data to predict the Probability of Default with much higher precision.

- Regulatory Compliance: Automation ensures that every loan application adheres to current banking norms, creating a digital audit trail for inspections.

👉 Want to see how Bank Statement Analysis Software can simplify your workflow? Try it now!

Implementing Automation: Moving Toward a Scalable LOS

To truly scale, your credit appraisal process cannot rely on hiring more people. It must rely on better systems. Integrating an automated appraisal tool into your existing Loan Origination System (LOS) creates a seamless, paperless loan processing workflow.

This shift allows your institution to handle 10x the volume of loan applications without increasing your headcount. It transforms the credit department from a cost center into a scalable revenue driver.

Conclusion: Speed is Your Best Marketing Tool

The future of lending is transparent, data-driven, and—above all—fast. By adopting automated credit appraisal, you aren’t just cutting down on paperwork; you are providing a better experience for your borrowers and a more secure framework for your stakeholders.

Don’t let manual spreadsheets hold your growth hostage. It’s time to automate the mundane and focus on what matters: making informed, profitable credit decisions.

Ready to slash your loan TAT?

Explore Pro Analyser and simplify your credit journey — Start today.