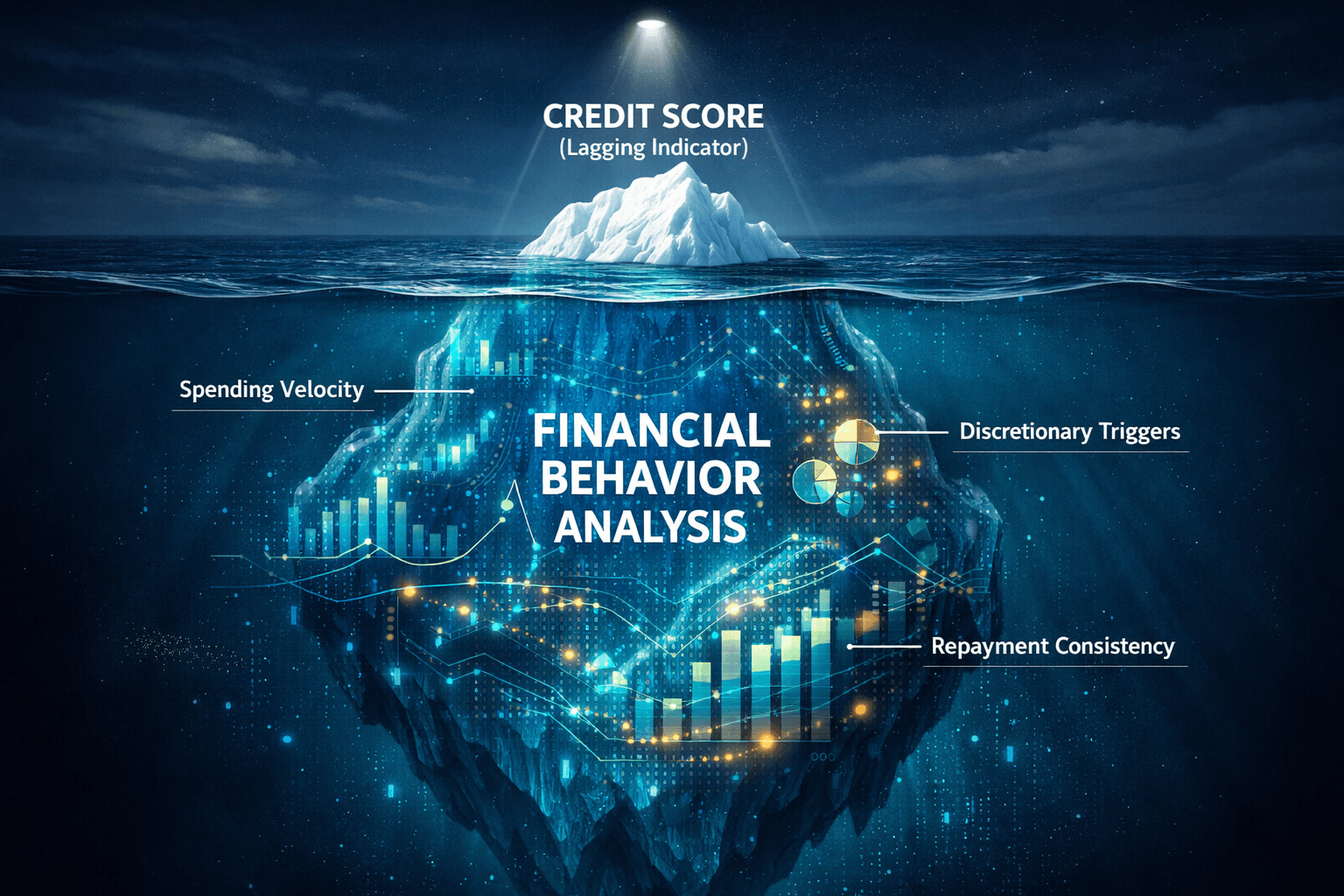

In the modern lending landscape, a credit score is a lagging indicator. It tells you what happened months ago, but it rarely predicts what will happen tomorrow. To gain a true competitive edge, financial institutions and fintechs are shifting their focus toward Financial Behaviour Analysis.

While traditional metrics provide a snapshot of the past, understanding the difference between credit scores and real-time bank statement analysis is essential for a 360-degree view of a borrower. By leveraging a sophisticated bank statement analyzer, firms can now move beyond simple “pass/fail” metrics and start understanding the psychological “why” behind every transaction.

Decoding the Transaction DNA

Most automated tools simply categorize a transaction as “Groceries” or “Rent.” However, true behavior analysis looks at the rhythm of these actions.

For instance, does a borrower pay their utility bills the moment they receive their salary, or do they wait until the final reminder? The former suggests a “Strategic Repayment” behaviour, while the latter might indicate “Liquidity Friction”—even if the balance is technically sufficient. When you perform a deep bank statement analysis, you aren’t just looking for numbers; you are looking for consistency, discipline, and emotional triggers in spending.

By identifying inconsistent spending habits, a bank statement analyser does more than assess risk; it acts as a primary defence to prevent loan fraud through smart data analysis.

The Three Pillars of Behavioural Insight

- Velocity of Spending: How quickly does the account balance deplete post-salary? High velocity often correlates with a lack of financial buffer, regardless of the income bracket.

- Spending Anomalies: Does the user have a “Weekend Spike” in discretionary spending? Identifying these patterns helps in assessing lifestyle stability.

- Commitment Ratio: Analyzing the ratio of fixed subscriptions and recurring mandates versus flexible spending.

To see how these behavioural insights fit into your overall digital lending workflow, explore our comprehensive bank statement analyser guide for modern finance professionals.

Why Automation is Non-Negotiable

Manual review is prone to human bias and fatigue. A digital bank statement analyser ensures that every data point is treated with mathematical objectivity.

Pro Analyser’s engine uses machine learning to identify these behavioral archetypes in seconds, allowing lenders to approve “thin-file” borrowers who have strong behavioral markers but low traditional credit history. By focusing on data intelligence rather than just data entry, you can build a high-trust relationship with your customers by understanding their needs and risks before they even manifest on a balance sheet.

The Bottom Line

The future of finance isn’t just about data; it’s about the interpretation of that data. Financial Behaviour Analysis is the key to unlocking sustainable growth and reducing defaults in an increasingly digital economy.

Curious about the behavioural profile of your current portfolio? Run a sample statement through Pro Analyser today.