Ever checked your bank statement and thought, “I earn well – so why did my loan get rejected?”

Often, the answer hides in your income ratio – that quiet percentage which tells lenders how stretched your finances really are.

Let’s unpack what an unhealthy income ratio means, how it appears in your bank statement, and how to fix it before it dents your loan eligibility.

1️⃣ What Exactly Is an Income Ratio?

Your income ratio shows how much of your monthly earnings go toward fixed obligations like EMIs, rent, and credit card bills.

It’s a snapshot of how balanced – or overburdened – your income really is.

Here’s the simple income ratio formula:

Income Ratio = (Total Monthly Obligations ÷ Total Monthly Income) × 100

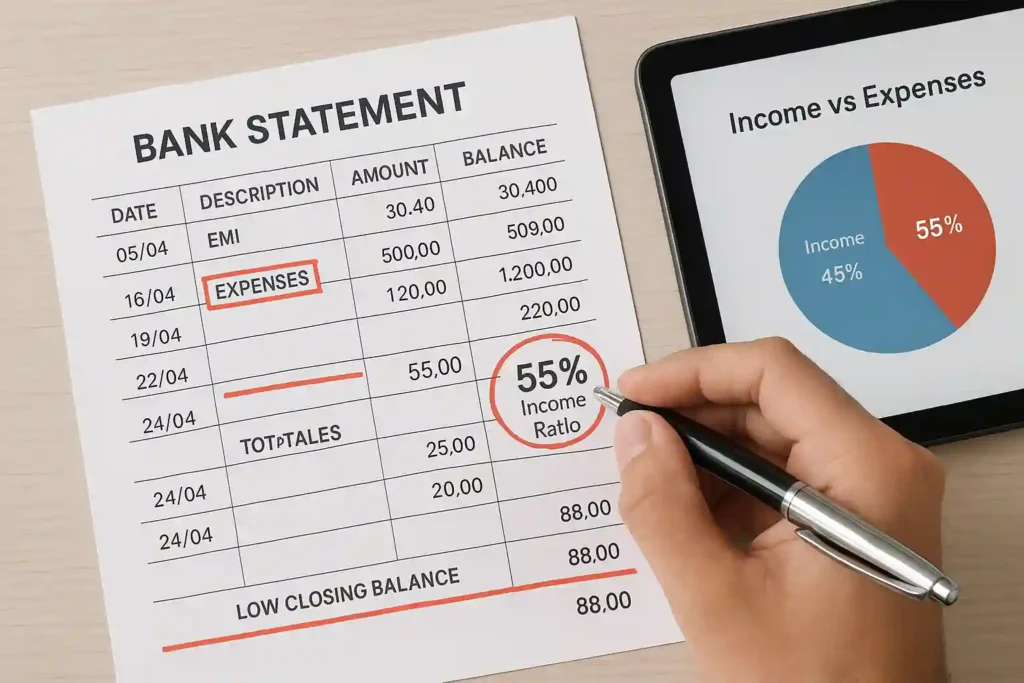

Example: If your income is ₹1,00,000 and your total EMIs are ₹55,000, your ratio is 55% — a level most banks consider risky.

A healthy range is generally below 50%, while anything above 55% suggests your financial commitments are too heavy.

Just divide your total monthly commitments by your total income. Simple math — or, if you prefer precision, an automated bank statement analysis software can handle it in seconds

2️⃣ How an Unhealthy Income Ratio Looks in Your Bank Statement

Your bank statement silently reveals your financial habits. Here’s what an unhealthy ratio looks like in real data:

- EMIs or card payments take up most of your income

- Salary credits are irregular or inconsistent

- Balances drop dangerously low before the next income credit

- Frequent overdrafts or cash advances

- Discretionary expenses (travel, dining, subscriptions) dominate spending

If you’ve read “5 Red Flags to Watch for in Bank Statements Before Approving a Loan,” you already know – these patterns trigger red alerts for lenders.

3️⃣ Why It Matters for Creditworthiness and Loan Approval

Financial institutions treat income ratio as a primary factor in creditworthiness analysis.

It directly affects loan eligibility and repayment confidence.

- Ratios above 55–60% usually flag high-risk profiles

- Affects loan approval time and overall credit score

- Even high earners can be declined if the ratio shows poor spending balance

For home loans, most lenders prefer a debt-to-income ratio below 45%. Beyond that, repayment reliability is questioned.

If you’re new to the lending process, you can explore our detailed article, “The Complete Loan Approval Process: Step-by-Step Guide for Lenders.”

4️⃣ Healthy vs. Unhealthy Income Ratio – A Quick Comparison

| Indicator | Healthy (Below 50%) | Unhealthy (Above 55%) |

|---|---|---|

| EMI Load | Balanced with income | Dominates monthly flow |

| Account Balance | Stable and surplus | Nearly empty before salary |

| Financial Stress | Manageable | High |

| Loan Approval | Strong | Weak |

Even if your income is high, poor expense control can distort this ratio – making your financial data appear unstable.

5️⃣ Common Financial Mistakes That Damage the Ratio

Surprisingly, the most common issues aren’t about income but behavior:

- Treating bonuses as guaranteed income

- Ignoring small EMIs and subscriptions

- Using multiple credit cards

- Not revising budgets after lifestyle changes

- Assuming “high income = good finances”

These habits inflate obligations and lower your real savings – damaging your financial data analysis picture.

6️⃣ How to Improve an Unhealthy Income Ratio

Good news: You can fix a bad ratio faster than you think.

Here’s what helps:

- Budgeting: Track your actual spending, not estimated amounts.

- Consolidate EMIs: One structured loan is easier to manage than five small ones.

- Cut Fixed Costs: Eliminate unused subscriptions and services.

- Income Planning: Find side income or recurring revenue sources.

- Automate Tracking: Use digital tools for consistent financial review.

Tip: Regularly monitoring your ratio helps prevent surprises during loan applications.

If you’d like to understand automation’s role, read our “Ultimate Bank Statement Analyser Guide.”

7️⃣ How Banks Verify Income Ratios

During loan processing, lenders assess:

- Your last 3–6 months of bank statements

- Salary slips and ITR filings

- Consistency between declared income and spending pattern

This is where ProAnalyser’s Bank Statement Analyser comes into play.

It automatically reviews inflows, EMIs, and expense trends – helping lenders perform faster and more accurate creditworthiness analysis.

For tax-linked verification, ITR Analyser simplifies the process further, ensuring income proof verification is quick and reliable.

(You can explore this in our article: Income Proof Verification for Loans: ITR Simplifies Lending)

8️⃣ How Automation Strengthens Financial Accuracy

Modern lenders don’t rely on manual checking anymore. Automated bank statement analysis software provides:

- Real-time expense-to-income visibility

- Pattern recognition for risky ratios

- Instant report generation for financial data analysis

- Clearer insights for both individuals and lending institutions

It’s faster, cleaner, and far more consistent than spreadsheet tracking.

9️⃣ FAQs – Quick Clarity on Common Queries

Tracking your ratio helps you understand how much of your earnings are tied up in obligations versus available for savings or investments. By monitoring it regularly, you can identify financial stress points, avoid over-leveraging, and improve your loan eligibility and overall creditworthiness.

To find your income ratio in a bank statement, review all regular inflows and compare them with recurring outflows like EMIs, subscriptions, and bills. Alternatively, you can use digital bank statement analysis tools to automate the calculation and instantly spot areas where your ratio is high.

For home loans, lenders generally prefer a debt-to-income ratio below 45%, meaning less than half of your income goes toward fixed obligations. Maintaining this ratio improves your loan eligibility and signals stable financial management to banks.

The cost-to-income ratio measures a bank’s operating efficiency by comparing expenses to total income. Banks typically maintain a ratio between 40–50%, balancing profitability with operational costs, and it indirectly reflects how efficiently your banking transactions are processed.

Improving a high income ratio involves reducing unnecessary fixed costs, consolidating high-interest debts, and creating a disciplined monthly budget. Monitoring spending with tools or software can help identify problem areas and restore a healthier balance faster.

🧭 Final Thoughts

An unhealthy income ratio doesn’t just impact loan eligibility – it reflects your financial discipline.

By controlling expenses, improving income planning, and using smart tools, you can bring it back to the safe zone.

Whether you’re applying for a loan or just want to stay financially balanced, tracking this ratio is the simplest step toward long-term financial health.