Ever seen two applicants with the same credit score — but one gets approved instantly while the other faces “further verification”?

That’s often because of one thing lenders don’t joke about: income proof for loan.

Your credit score may show how you repay.

But your income documents reveal if you can repay.

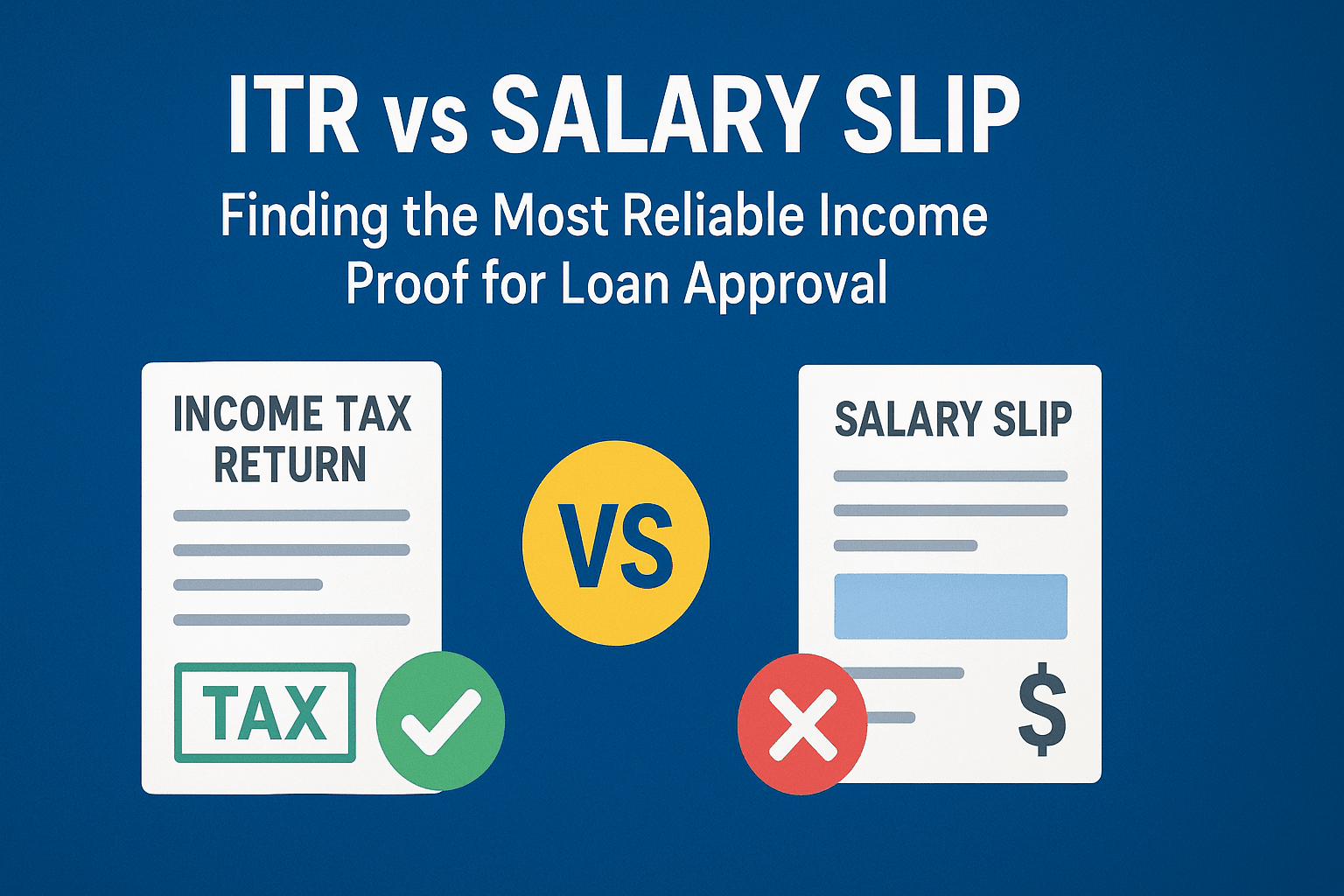

And when it comes to proving that, the debate always circles back to two names — ITR and salary slip.

So, which one do lenders actually trust more?

Let’s break it down.

Why Lenders Ask for Income Proof for Loan

Before a bank or NBFC releases even a rupee, they want assurance — real numbers that reflect earning stability.

That’s where income proof for loan becomes critical.

These documents help lenders:

- Measure repayment capacity

- Assess financial discipline

- Verify income sources

- Evaluate risk exposure

Think of them as the financial equivalent of a background check.

While credit reports show your past behavior, loan eligibility documents like ITRs and salary slips reveal your present financial standing.

For lenders, this combination is the foundation of a fair and transparent credit evaluation process in India.

You can also explore how digital lending platforms accelerate this with real-time analytics in our detailed post — Digital Lending 2.0: Faster, Safer Credit with GSTR Analysis.

Income Tax Returns (ITR): The Bigger Financial Picture

Why ITR Matters for Lenders

Your ITR isn’t just about taxes. It’s a full-year snapshot of your income — from salary, business, rent, or investments.

It reveals consistency, compliance, and transparency.

For self-employed professionals, ITRs act as primary proof of income. It’s their way of saying, “Hey lender, here’s my full income trail — all declared and verified.”

For deeper insights into this process, check out our guide — Pro Analyser ITR Verification in Loan Process Made Easy.

Pros and Cons of ITR as Income Proof

Pros:

- Covers multiple income sources

- Shows long-term financial reliability

- Indicates tax compliance

Cons:

- Updated only once a year — not real-time

- Some borrowers underreport income

- Manual verification can be slow

That’s why in the ITR vs salary slip for loan approval debate, ITRs score high on depth but lower on immediacy.

👉 Want to see how ITR Analysis Tool can simplify your document review and credit checks? Try it now!

Salary Slips: The Real-Time Snapshot

Why Lenders Value Salary Slips

Salary slips speak in real-time.

They show exactly what you earn, how often you’re paid, and what gets deducted.

For salaried professionals, these are the most accessible and verifiable income documents for credit evaluation.

If you’re interested in how automation speeds this up, you’ll enjoy our article on Income Verification: Fast & Secure Lending with Bank Statements.

Pros and Cons of Salary Slips

Pros:

- Up-to-date monthly record

- Easy for lenders to verify

- Great indicator of job stability

Cons:

- Limited to salaried individuals

- Doesn’t reflect side income or freelance earnings

- Forged slips are still a risk

That’s why lenders verify income today often involves fintech-powered data validation — tools that cross-check salary slips with bank statements and ITRs for accuracy.

For example, RBI and SEBI emphasize improved income verification methods in their compliance frameworks (Source: RBI | Source: SEBI).

ITR vs Salary Slip: Which Is Better for Loan Approval?

Here’s the short answer — neither alone paints the full picture.

ITRs provide the long-term, tax-backed perspective.

Salary slips provide short-term, real-time accuracy.

| Criteria | ITR | Salary Slip |

| Frequency | Annual | Monthly |

| Income Type | All sources | Salaried only |

| Ideal For | Self-employed | Salaried employees |

| Verification | Through tax records | Via employer/HR |

| Data Depth | Comprehensive | Current snapshot |

So, which is better for loan – ITR or salary slip?

It depends on who’s applying. Lenders often combine both to verify consistency and detect mismatches.

The Smarter Way: Digital Income Validation Tools

Manual verification used to take days.

Now, it takes minutes — thanks to fintech tools.

Modern lenders use digital solutions that automatically read and analyze ITRs, salary slips, and bank statements together.

This approach speeds up the credit evaluation process in India and reduces manual effort.

Tools like Bank Statement Analysers detect inflows, recurring credits, and unusual patterns — helping lenders confirm repayment ability instantly.

If you’d like a deeper dive into how this works, read our complete Bank Statement Analyser Guide.

Automation doesn’t just make it faster — it makes it smarter.

Connected Financial Analysis Tools That Strengthen Credit Evaluation

Financial truth doesn’t live in one document — it lives across many.

That’s why lenders today use multiple analysers that together create a full 360° profile of an applicant’s financial behavior.

1. Bank Statement Analyser (BSA)

Your BSA gives lenders an instant overview of cash inflows and outflows.

It verifies income stability, spending behavior, and unusual patterns in seconds.

🔗 Explore Bank Statement Analyser

2. GST Analyser

For business borrowers, GST filings reveal turnover consistency and tax compliance.

It ensures declared income aligns with actual business activity.

🔗 Explore GST Analyser

3. ITR Analyser

ITR data can be complex — but not when automated.

An advanced ITR Analysis solution simplifies extraction, organizes tax data, and highlights key indicators for quick verification.

Together, these tools make income verification seamless — helping lenders trust data, not documents.

Conclusion

Both ITR and salary slips play vital roles in income proof for loan evaluation.

One shows your financial roots, the other your current growth.

But when paired with automation through analysers, they become far more powerful — transparent, consistent, and easy to verify.

So whether you’re processing loans or applying for one, remember this:

Strong data builds stronger trust. And in lending, trust is everything.

👉 Simplify credit assessments today — explore our ITR Analyser and discover faster, data-driven lending decisions.