Goods and Services Tax (GST) reshaped India’s indirect tax landscape by unifying a maze of central and state levies into a single destination-based tax. This comprehensive guide explains what GST is, how a GST number works, and the practical impact of GST in India—across sectors and impact of GST on business decisions.

What Is GST?

GST is a destination-based, multi-stage indirect tax levied on the supply of goods and services. It aims to eliminate the cascading effect of multiple taxes (such as VAT, service tax, excise, octroi, and entry tax) by enabling input tax credit (ITC) across the value chain.

Key structural elements:

- CGST and SGST/UTGST apply to intrastate supplies; IGST applies to interstate supplies.

- Input Tax Credit allows businesses to offset taxes paid on inputs against output liabilities, subject to eligibility and documentation.

- Threshold-based registration is required for businesses exceeding prescribed turnover limits, with a composition scheme available for eligible small taxpayers (at lower tax rates but without ITC on outward supplies).

Why it matters:

- Reduces tax cascading and increases transparency.

- Digitizes compliance via standardized returns, e-invoicing, and e-way bills.

- Creates a more unified market, simplifying interstate trade and logistics.

Many businesses pair basic compliance with periodic GST analysis to spot credit leakages and use a GST tool for faster filings and GST verification of counterparties.

What Is a GST Number (GSTIN)?

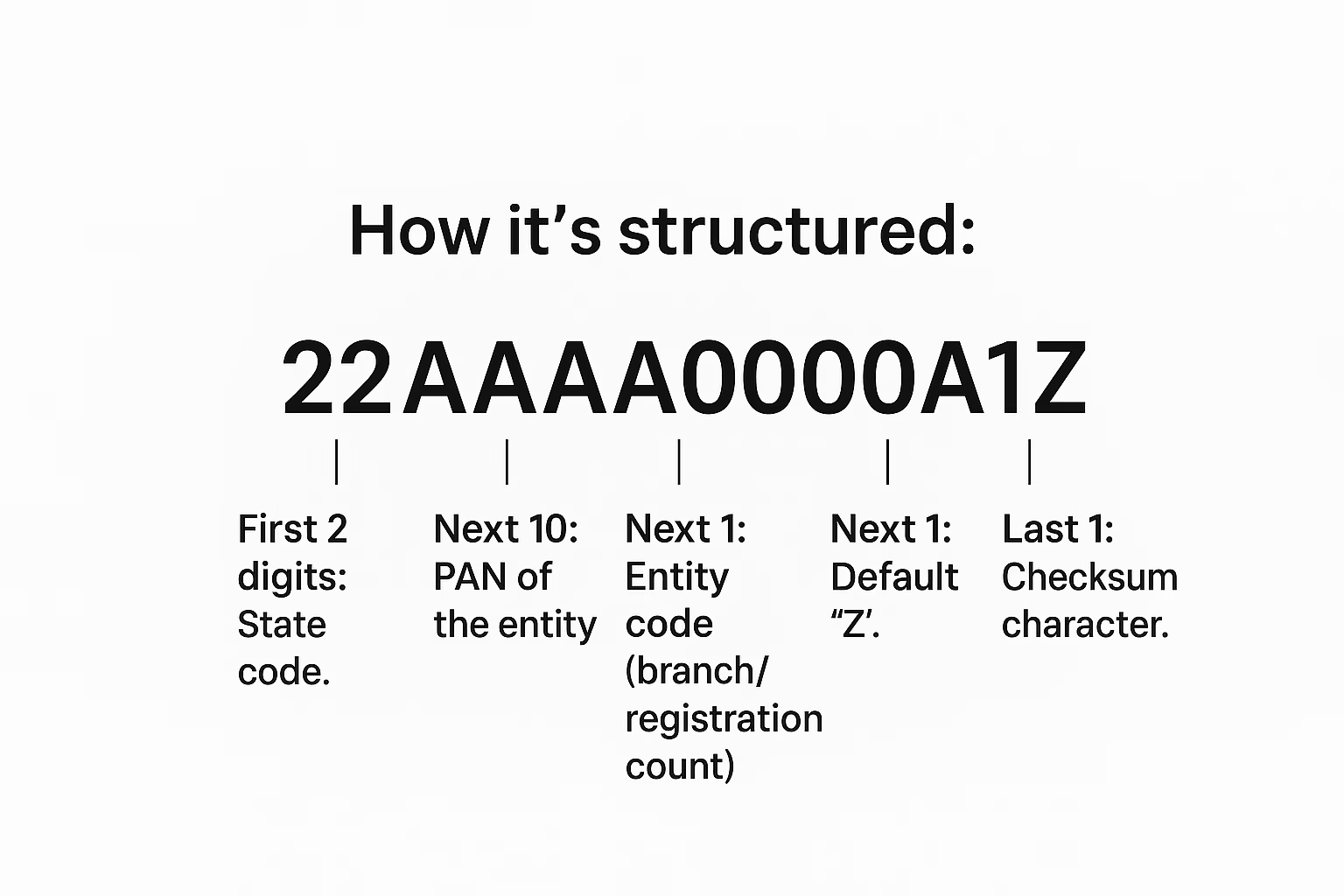

A GST number (GSTIN) is a 15‑digit unique ID assigned to every taxpayer registered under India’s Goods and Services Tax. Its structure is:

- First 2 digits: State code

- Next 10 digits: PAN of the taxpayer

- Next 1 digit: Entity code (registration number for that PAN in the state)

- Next 1 character: Default “Z”

- Last 1 character: Checksum

The GSTIN appears on invoices, returns, and e‑way bills, and is essential for compliance, input tax credit, and supplier verification. Verification can be done on the GST portal by searching a GSTIN before onboarding vendors.

Before onboarding suppliers, conduct GST verification on the portal or via a trusted GST Analysis tool to reduce ITC risks and onboarding delays.

Impact of GST in India: The Big Picture

GST has unified India’s indirect tax system, and the impact of GST is visible in better transparency and logistics alongside new compliance and cash‑flow realities for businesses. Below we have discussed some,

- Market unification: Replaces fragmented state/central taxes with a harmonized structure, easing interstate trade.

- Transparency and traceability: Invoice-level reporting, e-way bills, and e-invoicing enhance audit trails and reduce evasion.

- Formalization: Wider registration base brings more businesses into the formal economy, improving credit access and vendor credibility.

- Logistics efficiency: Removal of check posts and standardized documentation reduces transit time and costs.

- Revenue and compliance modernization: Digital filings and analytics-driven administration improve oversight but increase process rigor.

- Transitional realities: Frequent rule/rate changes and ITC constraints create a learning curve and cash-flow considerations.

Impact of GST on Business

Compliance

- Registration: Mandatory once turnover crosses thresholds; separate state-wise registrations for fixed establishments.

- Returns: Periodic filings (e.g., outward supplies and summary returns), with reconciliations against vendor-reported data.

- E-invoicing and e-way bills: Required above notified turnover thresholds and consignment values, respectively.

Cash flow and ITC

- ITC reduces tax cost but depends on vendor compliance, invoice accuracy, and eligibility rules.

- Timing differences, blocked credits, and mismatches can lock working capital and create interest exposure.

Pricing and margins

- With cascading reduced, pricing can be more transparent; however, classification, exemptions, and cess can influence effective tax rates.

- Businesses often realign pricing strategies to reflect ITC availability and sector-specific restrictions.

Procurement and vendor management

- Preference for compliant vendors to protect ITC.

- Contract clauses often include GST compliance warranties, indemnities for ITC denials, and timelines for invoice upload.

Technology enablement

- ERP/accounting integration for invoice generation, e-invoice IRN/QR flows, and automated reconciliations is now a competitive necessity.

Risk and penalties

- Interest on delayed tax, penalties for incorrect filings, and potential registration suspension/cancellation for defaults.

- Strong internal controls and periodic audits reduce exposure.

Practical tips

- Automate vendor and GSTR-2B reconciliation monthly.

- Maintain a robust HSN/SAC master and update for rate/notification changes.

- Document ITC eligibility, reversals, and vendor follow-ups to withstand audit.

To uncover hidden mismatches and credit leakages, explore common patterns in GST data and ITC risks flagged by smart analysis.

Impact of GST in Different Sectors

Manufacturing

- Benefits: Lower cascading, better interstate logistics, and clearer tax credits on inputs/capital goods.

- Considerations: Cash-flow planning for ITC accumulation; accurate classification for rate and cess.

E-commerce

- Operator obligations such as TCS and mandatory registration thresholds for platforms.

- Simplified pan-India sales, but increased reconciliation across orders, returns, cancellations, and refunds.

MSMEs

- Composition schemes can reduce tax rates and compliance, but restricts ITC and B2B competitiveness.

- Digital compliance requires adopting software and processes; outsourcing can help bridge capabilities.

Services/IT

- Place-of-supply rules drive tax type (IGST vs CGST/SGST) and registration needs.

- Multi-state operations may require multiple registrations and establishment-level compliance.

Logistics

- E-way bills and uniform rules reduce transit delays and optimize fleet utilization.

- Strong documentation discipline is essential to avoid detention/penalties during transit checks.

Real estate and construction

- Rate changes and project-based rules over time; limited ITC in certain residential projects affects costing.

- Reverse charge on specified services; meticulous project accounting is key.

Automotive

- Consolidation of taxes simplified ex-showroom pricing; compensation cess applicable for certain vehicle types.

- ITC on parts and spares is critical to dealer margins; robust stock and ITC control needed.

Hospitality and restaurants

- Rate slabs and ITC restrictions for some categories affect menu pricing and profitability.

- Clear invoicing and eligibility tracking for mixed supplies (rooms, F&B, services).

Pharma and healthcare

- Many core healthcare services are exempt, leading to blocked ITC on inputs; cost absorption/planning required.

- Pharma manufacturing benefits from supply-chain credits and standardized logistics.

Benefits and Challenges of GST

Benefits

- Unified national market and reduced tax cascading.

- Enhanced transparency and traceability through digital compliance.

- Supply-chain and logistics efficiencies, aiding competitiveness and ease of doing business.

Challenges

- Frequent updates to rules, rates, and procedures.

- ITC eligibility restrictions, vendor dependency, and reconciliation workload.

- Compliance complexity for small businesses without systems or trained staff.

How to Register for GST and Get a GST Number

Eligibility and options

- Registration required when turnover exceeds notified thresholds; voluntary registration available to avail ITC and formalize operations.

- Composition scheme for eligible small taxpayers (turnover limits apply), with lower rates and reduced compliance, but no ITC on outward supplies.

Documents typically required

- PAN, proof of business constitution (partnership deed, incorporation certificate), address proof of the principal place of business, bank details, photographs, and authorization/board resolution.

Step-by-step process

- Initiate new registration on the GST portal.

- Verify via OTP to generate a Temporary Reference Number (TRN).

- Complete the application with business details and upload documents.

- Submit and track using the Application Reference Number (ARN).

- Respond to any clarifications and receive GSTIN upon approval.

Post-registration setup

- Add additional places of business, HSN/SAC, and bank validation.

- Configure e-invoicing if turnover threshold applies; set up e-way bill credentials.

- Align ERP/accounting masters, invoice formats, and compliance calendars.

Managing GST Compliance: A Quick Checklist

- Maintain accurate legal and master data (name, trade name, addresses, bank, HSN/SAC).

- Classify supplies properly and monitor exemptions and reverse charge mechanisms (RCM).

- Reconcile GSTR-2B with the purchase register every month; follow up on missing/incorrect invoices.

- File outward supplies and summary returns on time; pay tax and interest if due.

- Generate e-invoices and e-way bills where applicable; ensure QR codes/IRN details are present.

- Preserve records: invoices, e-invoices, e-way bills, ledgers, returns, ITC workings, and correspondence.

- Conduct periodic internal GST audits and mock assessments.

For a step‑by‑step playbook on filings, e‑invoicing, and ITC hygiene, see our GST compliance guide for 2025.

Ready to simplify compliance? Explore our GST Analysis with built‑in GST verification and one‑click GST analysis to accelerate monthly filings.

FAQs

Yes, once turnover crosses specified thresholds; some businesses register voluntarily to avail ITC or supply inter-state/B2B.

CGST and SGST/UTGST apply to intrastate supplies and are shared between Centre and State; IGST applies to interstate and imports, later apportioned.

Generally yes, subject to eligibility, usage for taxable supplies, and documentation; certain blocked credits apply.

ITC may be restricted or delayed; follow up with the vendor, reconcile discrepancies, and consider contractual safeguards.

E-invoicing applies above notified aggregate turnover thresholds; businesses should confirm their status each time thresholds are revised.

Exports are treated as zero-rated supplies; exporters may supply under bond/LUT without payment of tax or pay IGST and claim a refund, subject to procedures.