In today’s fast-paced lending environment, knowing how to analyse bank statements is no longer optional — it is a core competency for every NBFC, lender, and credit professional. Whether you are processing retail loans, MSME credit, or personal finance products, the bank statement tells a story that no other document can. It reveals a borrower’s income patterns, spending behaviour, repayment history, and overall financial discipline — all in one place.

This guide breaks down the fundamentals of bank statement analysis, why it matters for modern lenders, and how smart bank statement analysis tools are transforming the credit underwriting process.

What Is Bank Statement Analysis?

Bank statement analysis is the process of systematically reviewing a borrower’s bank account transactions over a defined period — typically 3 to 12 months — to assess their financial health, income consistency, and creditworthiness.

A thorough analysis typically covers:

- Income credits — salary, business receipts, rental income, or freelance payments

- Fixed obligations — EMI debits, insurance premiums, and loan repayments

- Average monthly balance (AMB) — a key indicator of financial stability

- Bounce rate — frequency of returned cheques or failed ECS/NACH mandates

- Spending patterns — discretionary vs. essential expenditure

- Cash flow irregularities — sudden large withdrawals or unexplained deposits

Together, these data points paint a 360-degree picture of the applicant’s financial behaviour — far more nuanced than what a credit bureau report alone can provide.

Why Does It Matter for NBFCs and Lenders?

For NBFCs and lending institutions, credit decisions are high-stakes. A single misjudged loan can result in significant NPA (non-performing asset) risk. This is where bank statement analysis becomes indispensable. Here is why:

1. Income Verification Beyond Pay Slips

For salaried professionals, pay slips can be forged or inflated. Bank statements provide ground truth. Regular, consistent salary credits from an identified employer confirm actual take-home income. For self-employed borrowers or business owners, cash flow patterns in the bank account serve as the primary income proof.

2. Identifying Hidden Liabilities

Borrowers may not disclose all existing EMIs in their loan application. Bank statement analysis can expose undisclosed debt obligations through recurring debits — giving lenders a true picture of the applicant’s debt-to-income (DTI) ratio.

3. Detecting Early Stress Signals

Repeated cheque bounces, falling average balances, or a sudden surge in cash withdrawals are early warning signs of financial stress. Identifying these red flags at the underwriting stage helps lenders avoid future defaults. To understand how NBFCs specifically use these signals to strengthen their credit process, read our detailed guide on bank statement analysis for NBFCs.

4. Enabling Faster, Data-Driven Decisions

Manual review of bank statements is time-consuming and error-prone. In a competitive lending market, speed is a differentiator. Automated bank statement analyser enables credit teams to process higher volumes with greater accuracy and consistency.

How to Analyse Bank Statements: A Step-by-Step Approach

Understanding how to analyse bank statements effectively involves a structured workflow:

Step 1 — Collect and Authenticate: Obtain 6–12 months of bank statements directly from the borrower or via account aggregator. Verify authenticity by checking for tampering, consistent formatting, and matching account details.

Step 2 — Categorise Transactions: Classify all credits (income sources) and debits (expenses, EMIs, utilities) into meaningful categories. This reveals spending priorities and fixed obligations.

Step 3 — Calculate Key Metrics: Compute average monthly balance, total inflows, total outflows, EMI obligations, and bounce rate. These are your primary underwriting parameters.

Step 4 — Identify Patterns and Anomalies: Look for consistency in salary credits, unexplained large deposits (potential loan stacking), or irregular debit patterns that suggest financial distress. A strong way to validate these patterns is by examining cash flow trends over time — explore how cash flow analysis using bank statements helps lenders build a more accurate and defensible borrower profile.

Step 5 — Generate Credit Insights: Consolidate findings into a structured credit note or scorecard that supports the loan sanctioning decision.

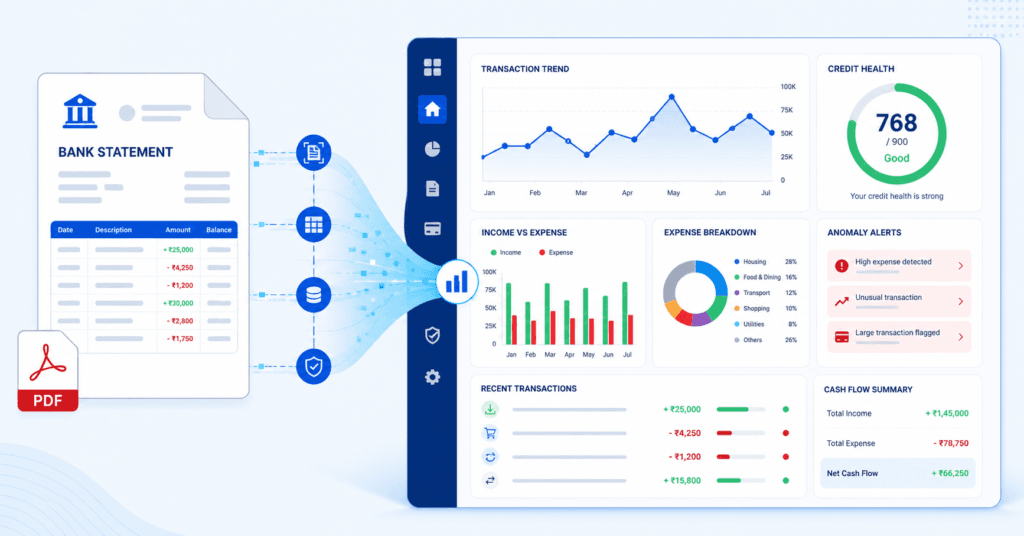

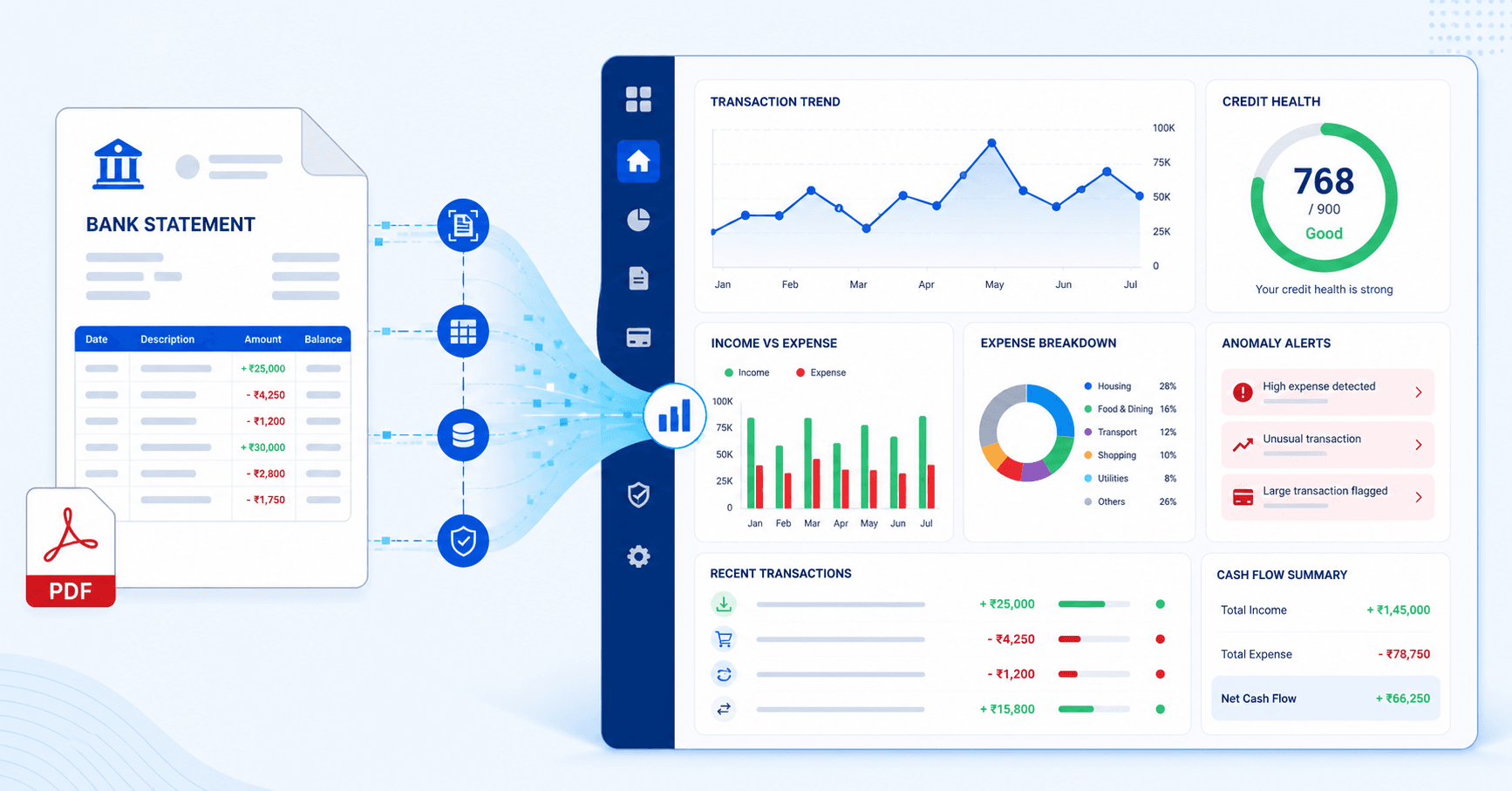

The Role of a Bank Statement Analyser in Modern Lending

Doing all of the above manually for hundreds of loan applications every month is neither scalable nor sustainable. This is where a purpose-built bank statement analyser makes all the difference.

A modern bank statement analyser automates the entire workflow — from PDF parsing and transaction categorisation to anomaly detection and report generation. It eliminates manual effort, reduces processing time from hours to minutes, and ensures that every application is evaluated against a consistent, unbiased framework.

Today, AI is taking this a step further. If you want to see how artificial intelligence is changing the way lenders approach statement review, explore our post on how to analyze bank statements for loans using AI — and why smart lenders are making the switch.

At Pro Analyser, our platform is built specifically for the needs of NBFCs, banks, and lending institutions. It handles multi-bank statements, detects fraudulent patterns, and delivers structured, audit-ready reports — all with a few clicks.

Conclusion

Bank statement analysis is one of the most powerful tools in a lender’s underwriting arsenal. It goes beyond credit scores and documents to reveal the true financial reality of a borrower. For NBFCs and financial institutions aiming to reduce defaults, improve turnaround times, and scale responsibly, mastering how to analyse bank statements — or better yet, automating the process — is no longer a choice but a competitive necessity.

Ready to transform your credit underwriting process? Explore how Pro Analyser’s bank statement analyser can help your team make faster, smarter lending decisions.