Introduction

The loan approval process is the backbone of modern lending. For lenders, it’s not just about disbursing money-it’s about evaluating risk, maintaining compliance, and ensuring repayment. For borrowers, it’s the path that decides whether their financial plans move forward or hit a dead end.

Today, with digital tools, AI, and automated workflows, the process of loan approval has become faster, more transparent, and data-driven. But to understand how to optimize it, lenders need to break it down step by step.

What Is Loan Approval Process?

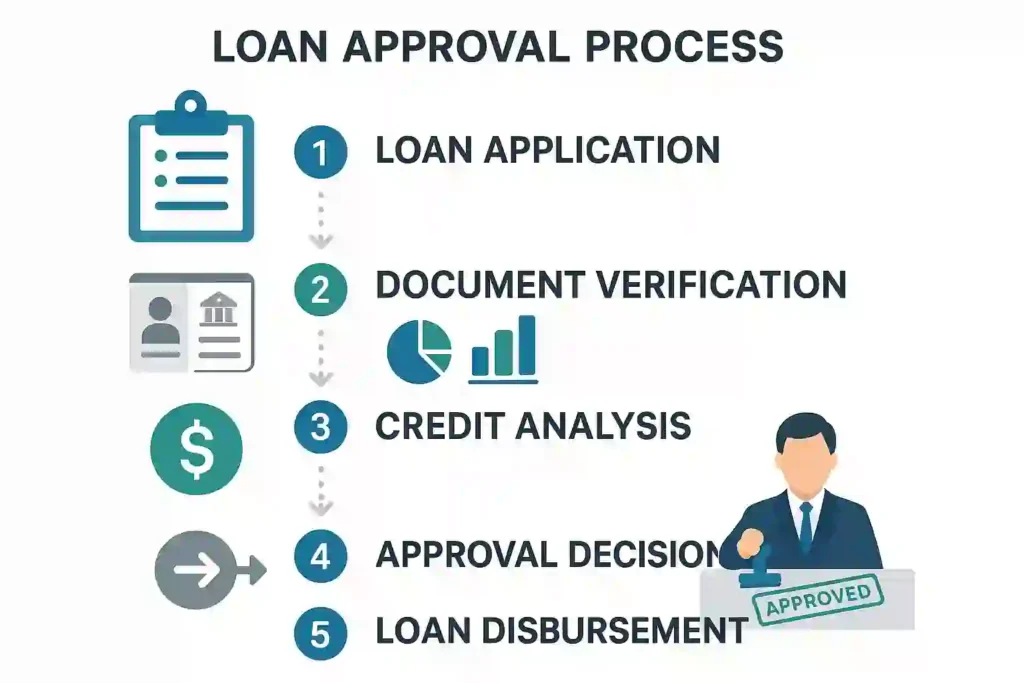

In simple terms, the loan approval process is the structured journey that a lender follows before deciding whether to fund a borrower. It involves verifying identity, reviewing income, analyzing risk, and finally issuing a decision.

Think of it like boarding a plane: passengers (borrowers) must pass through security checks (creditworthiness), show identification (KYC), and prove they’re fit to travel (financial health). Only then do they get a seat on the flight (loan disbursement).

Step 1: Loan Application

The process begins with the borrower submitting an application. This can happen online, via mobile banking, or at a physical branch.

Key borrower details collected include:

- Personal details (name, address, contact information)

- Employment and income information

- Requested loan amount and purpose

- Bank statements and supporting financial documents

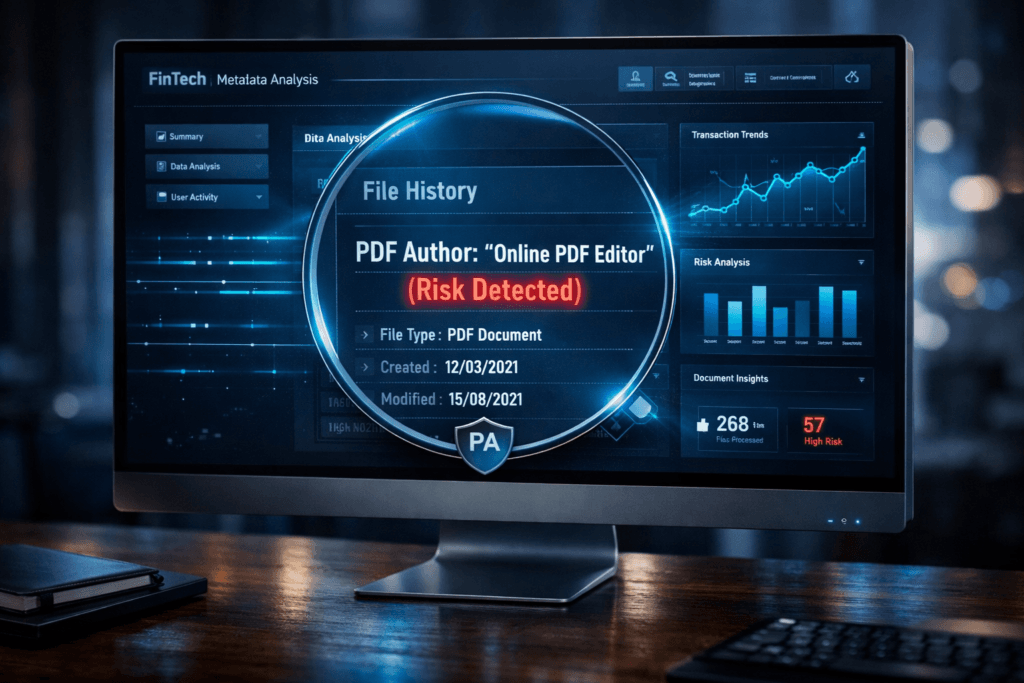

📌 At this stage, lenders already prepare for deeper checks. A good bank statement analysis software can immediately flag inconsistencies in income or suspicious inflows, making early screening faster.

Step 2: Document Collection and Verification

Once the application is in, lenders need to confirm the authenticity of documents.

Typical documents include:

- ID proof and KYC records

- Salary slips or income tax returns

- Bank statements (often 6–12 months)

- Business registrations for entrepreneurs

Here’s where bank statement analysis tools come into play. They simplify the analyse of bank statement by automatically categorizing inflows and outflows, highlighting regular patterns, and exposing possible manipulation.

This is also the stage where fraud can creep in. As one of your related blogs points out, lenders must watch for red flags in bank statements before approving loans.

Step 3: Creditworthiness and Risk Assessment

This is often the most critical phase. Lenders want to ensure that the borrower has the capacity and intent to repay.

What’s usually checked:

- Credit score and repayment history

- Debt-to-income ratio

- Stability of employment or business revenue

- Loan-to-value ratio for secured loans

Traditionally, this was manual and time-consuming. But with AI, things are changing fast. As we covered in our blog on how AI is changing the way lenders use bank statements for loan, lenders can now process huge data sets instantly. AI models spot unusual spending, detect hidden liabilities, and even predict repayment behavior.

This is also where automated loan assessment solutions are gaining ground. Instead of waiting days, decisions can be made in hours—or even minutes.

Step 4: Loan Approval Workflow and Underwriting

If the borrower passes credit checks, the application enters the loan approval workflow. Underwriters review the information and assign a risk grade.

Underwriting involves:

- Final verification of documents

- Cross-checking borrower declarations

- Risk scoring and loan pricing

- Compliance with lending policies and regulations

In many institutions, this is still partly manual. But lenders are increasingly adopting documents processing with AI to speed up the cycle without losing accuracy.

If you’re looking for a quick overview, our blog on Loan Approval Workflow: From Application to Decision breaks down the essentials in a simplified format. But here, let’s go deeper into the strategic details lenders need to know

Step 5: Decision and Communication

Once underwriting is complete, the lender issues a decision: approved, rejected, or conditionally approved.

For approved loans, the borrower receives a sanction letter that includes:

- Loan amount

- Interest rate and tenure

- Repayment schedule

- Terms and conditions

Rejected applications often come with reasons such as low credit score, unstable income, or insufficient documentation. Here, clear communication matters. Borrowers appreciate transparency, and lenders build long-term trust.

Step 6: Loan Disbursement

After acceptance of terms, funds are disbursed into the borrower’s account. This is the final stage, but it doesn’t mean the lender’s job is over. Continuous monitoring is essential to detect signs of loan processing workflow inefficiencies or risks.

Smart lenders also implement early warning systems to prevent loan fraud by tracking unusual repayment behaviors or sudden cash flow shifts.

Benefits of Streamlining the Loan Approval Process

A well-defined process benefits both lenders and borrowers.

For lenders:

- Reduced risk of default

- Faster turnaround times

- Compliance and audit readiness

- Cost savings from automation

For borrowers:

- Quicker decisions and access to funds

- Better customer experience

- Transparent communication

- Confidence in the fairness of the process

Challenges and Best Practices

Even the most refined approval systems face challenges:

- Fraudulent documents and identity theft

- Ambiguous financial transactions

- Overreliance on manual reviews

- Data privacy and regulatory compliance

Best practices for lenders include:

- Leveraging AI and automation wherever possible

- Maintaining human oversight for borderline cases

- Updating risk models regularly

- Integrating with APIs for instant verification

- Referring to resources like your ultimate guide for bank statement analyser for deeper insights

Future of Loan Approvals

The future of lending will be shaped by technology. AI, open banking APIs, and real-time analytics will make approvals faster and smarter. We’ll see deeper integration of trends in bank statement analysis, predictive modeling, and borrower segmentation.

Instead of waiting weeks, borrowers could receive decisions in seconds. And instead of relying on outdated PDFs, lenders will rely on continuous data feeds.

Conclusion

The loan approval process may look complex, but with the right structure and tools, it becomes a powerful engine for growth. From application to disbursement, each step matters—not just for compliance, but for building borrower trust.

By adopting automation, using bank statement analysis software, and embracing AI, lenders can cut costs, improve accuracy, and deliver a seamless borrower experience. In short, the process of loan approval is no longer just paperwork-it’s a competitive advantage.