Why This Integration Matters

Every lender faces the same puzzle: How do you know if someone will repay? Traditional credit scores give one clue-borrower discipline in handling past loans. Bank statement analysis gives another-actual cash flow, spending, and income consistency.

When you combine these two, you get something powerful: a 360-degree borrower profile. A person with thin or no credit history can finally be assessed fairly if their statements show healthy inflows. On the other hand, someone with a decent score but heavy EMI outflows can be flagged before defaults pile up.

The result? Faster approvals, smarter risk management, and fewer defaults.

This isn’t theory. Fintech lenders, NBFCs, and even large banks are already embedding bank statement analyser APIs with credit scoring APIs in their tech stack. Let’s break down how it actually works.

The Tech Stack in Action

Behind every quick “approved” or “rejected” decision is a detailed workflow running in the background. What looks simple to a borrower is actually a carefully designed pipeline that connects multiple systems.

| Step | What Happens | Tools Commonly Used |

| 1 | Raw statements ingested from borrowers (PDFs, email, or aggregator feeds) | Bank Statement Analyzer API |

| 2 | Transactions cleaned, categorized into income, EMI, spends, anomalies | Python, Node.js, Java middleware |

| 3 | Credit score fetched from bureau | Experian, CIBIL, CRIF APIs |

| 4 | Data merged into decision engine | Loan underwriting software, risk models |

| 5 | Decision triggered (approve, reject, manual review) | Loan decisioning engine |

Notice that both APIs-BSA and credit scoring-don’t work in silos. The orchestration layer (middleware) is where the magic happens. That’s where developers normalize data, align schemas, and feed results into a single dashboard for credit officers.

👉 Expert Tip: Always design the middleware to be “vendor-neutral.” If your primary bureau API goes offline, your system should automatically fall back to a secondary provider without disrupting approvals.

Why Lenders Struggle with Integration

On paper, it all seems straightforward. But when lenders actually attempt to stitch BSAs and bureau APIs together, they run into recurring hurdles that can slow projects or even stall adoption.

-

Data Mapping Conflicts

Different BSAs label fields differently. One tags salary credit, another calls it income inflow. If your integration doesn’t reconcile these, you’ll get broken borrower profiles. -

Latency & Downtime

Credit bureau APIs are not always instant. A slow or failed call during an online loan application can cause customer drop-offs. -

Security & Compliance

Borrower statements and credit scores are both highly sensitive. If data is exposed during transfer, you risk legal penalties and reputational damage. -

Interoperability Issues

APIs from different vendors “speak different languages.” Some return JSON, others XML. Some use detailed categories, others provide raw dumps. Orchestration becomes tricky.

This is where many lenders pause-because integrating multiple financial APIs is not just a tech project, it’s a compliance and reliability challenge.

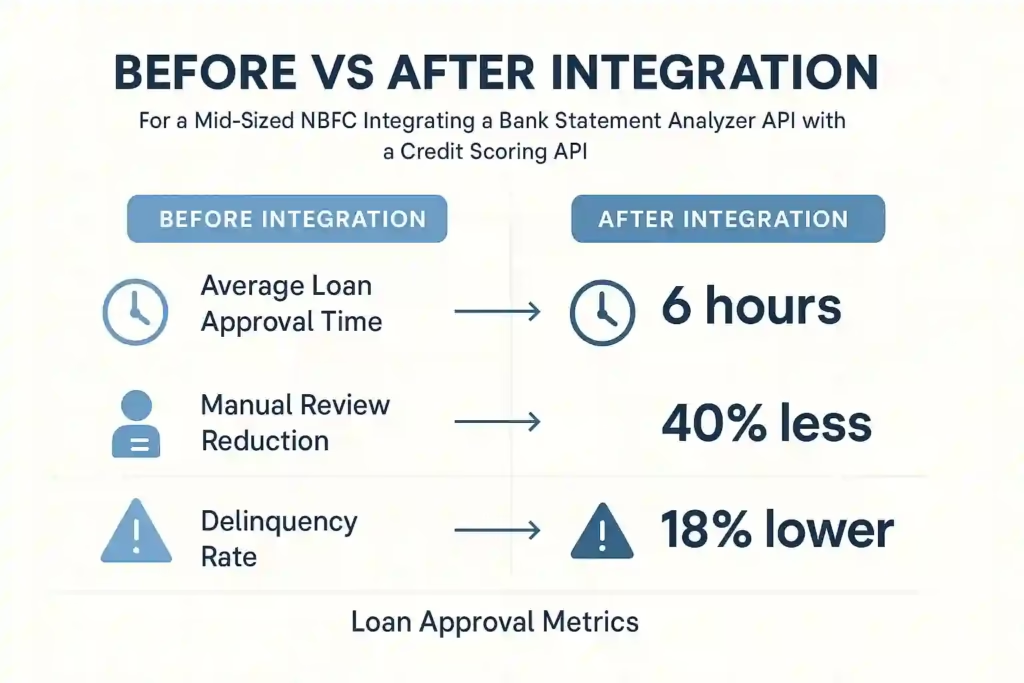

Real-World Example

A mid-sized NBFC in South India was approving loans the old-fashioned way-statement checks in Excel + bureau pull in a separate workflow. The average approval time was 48 hours, and many “credit invisible” applicants were rejected.

After they integrated their bank statement analyser API with a credit bureau API, the workflow changed:

- Approvals dropped to under 6 hours.

- Manual reviews reduced by 40%.

- Delinquency rates fell by 18% in just six months.

What made the difference? The decisioning engine could now spot borrowers who looked fine on bureau scores but had heavy EMI burdens or frequent cheque bounces visible in their statements.

How Lenders Solve It

The good news is-these problems aren’t unsolvable. Many fintechs and banks have already figured out practical ways to overcome them without slowing their workflows.

-

Standardized Schemas

Before integration, align how key fields-income, EMI, bounced cheque-are named and structured. -

Retry & Failover Logic

Build logic that retries failed bureau calls or switches to another provider seamlessly. -

Security First

Always encrypt sensitive data. Use tokenization to avoid storing raw financial details longer than needed. -

Unified Internal API

Instead of connecting every app to every vendor directly, some fintechs create an internal unified API layer. That way, your lending engine doesn’t care if the data came from Experian, CRIF, or a specific BSA vendor.

The Bigger Picture: AI-Powered Lending

Integration today is just step one. The real transformation lies in how AI combines cash-flow data and credit bureau information into one smart score.

-

Better borrower profiles: AI learns patterns humans miss.

-

Fairness for thin-file borrowers: A healthy bank statement can balance out a low or non-existent credit score.

-

Real-time approvals: No more waiting for batch reports-AI-driven APIs deliver instant results.

India’s Account Aggregator framework will push this future faster. With customer consent, lenders will get verified data streams-statements, investments, even tax records-creating a single, secure, and highly accurate risk model.

Connecting the Dots

If you’ve read our Bank Statement Ultimate Guide , you know why BSAs are foundational for lending. Pair that with Integrating Bank Statement Analyzer API with Core Lending Platforms: A 360-Degree Deep Dive, and you see the operational backbone.

This blog is the missing piece-it shows how credit scoring APIs complete the picture. And if you’re curious about the next leap, Exploring the Role of AI in Banking and Financial Services paints the future of lending automation.

Internal linking like this ensures you don’t just understand one tool, but the entire ecosystem.

FAQs

Final Thoughts

In lending, time is money – and risk is everything. By integrating a bank statement analysis API with a credit scoring API, lenders gain faster workflows, sharper insights, and stronger protection against defaults.

The lenders who adopt this now will have a massive competitive edge. The ones who don’t? They’ll be stuck with outdated, manual processes while the market races ahead.