The lending industry is no stranger to change. From paper-based ledgers to digital platforms, every shift has aimed at making decisions faster, fairer, and more accurate. But today, the real turning point comes with AI in lending, especially when comparing manual vs automated bank statement analysis.

A lender’s success depends on spotting reliable borrowers quickly while catching red flags like fraudulent statements. That’s where automation and AI are quietly reshaping the future. Let’s break it down.

Why Bank Statement Analysis Matters More Than Ever

In a digital-first lending world, speed and accuracy decide who wins. A survey by McKinsey revealed that lenders using AI tools cut loan processing times by 60% while improving fraud detection by 30%.

For years, lenders relied on manual checks. Staff would review months of statements line by line-slow, error-prone, and expensive. But with modern bank statement analyser tools, a process that once took hours now takes minutes.

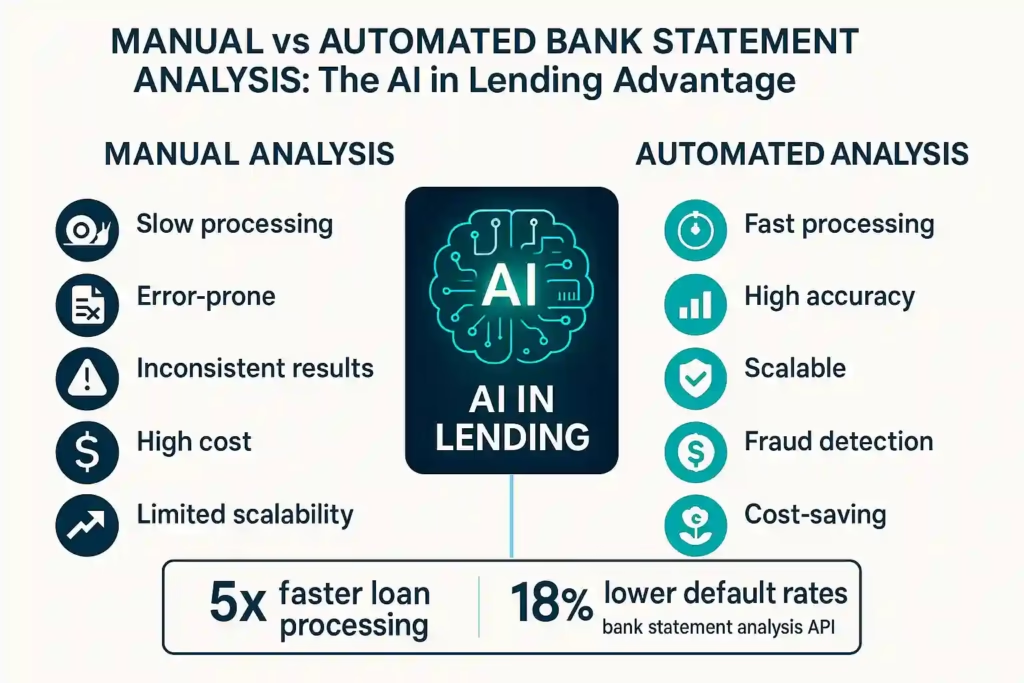

Manual Bank Statement Analysis: The Old Way

Even though manual reviews may sound traditional, they still exist across many mid-sized lending firms. Here’s why:

-

Human interpretation: Credit officers can add context, like unusual seasonal spending.

-

Flexibility: Works when formats are messy or when AI tools don’t integrate well.

-

Low-tech entry point: No heavy investment in new systems.

But it comes with big drawbacks:

- Time-intensive and inconsistent across officers.

- Higher error risk from human oversight.

- Difficult to scale as application volumes rise.

👉 Manual analysis is like driving with a map-you’ll eventually reach the destination, but it’s slow and full of stops.

Automated Bank Statement Analysis: Speed Meets Precision

Automation, backed by AI, changes the equation completely. Lenders using automated tools report processing up to 5x more applications per day. It’s not just about speed-it’s about quality insights.

-

Data accuracy: AI models detect income patterns, spending habits, and anomalies instantly.

-

Scalability: Thousands of statements processed without adding new staff.

-

Fraud detection: Advanced systems catch manipulated PDFs or unusual cash flows.

-

Compliance-ready: Outputs integrate directly into credit decision platforms.

👉 In fact, one leading fintech reported that integrating a bank statement analysis API reduced their loan default rate by 18% within the first year.

Manual vs Automated: Which Fits Lenders Best?

Every lender is at a different stage. Some may still rely on manual methods for specific cases. But for modern, digital-first lenders, automation offers clear benefits.

- Manual = control, but slower and riskier.

- Automated = faster, more accurate, and scalable.

- Hybrid = best of both worlds for firms transitioning to AI-powered workflows.

👉 If you’d like a deep-dive comparison, you can explore our Ultimate Bank Statement Analyser Guide which maps out the full picture with practical workflows.

How AI in Lending Expands the Impact

The shift isn’t just about replacing manual work-it’s about reimagining lending with AI at its core. Here’s what AI adds:

-

Loan approval accuracy: AI learns from historical repayment data to score borrowers more precisely.

-

Fraud detection: AI flags suspicious deposits or fabricated entries invisible to the human eye.

-

Credit scoring innovation: Goes beyond traditional credit scores by analyzing real-time cash flow.

Stat to note: According to Deloitte, AI-driven credit scoring models improve prediction accuracy by 20–30% compared to legacy systems.

👉 Curious about the bigger picture? Check out Exploring the Role of AI in Banking and Financial Services where we dive into how AI is remaking everything from risk assessment to customer experience.

The Future: AI Agents and Document Processing

As AI evolves, automated analysis will go beyond bank statements. Intelligent document agents can parse invoices, payslips, and tax returns, creating a 360° borrower view in seconds.

-

End-to-end automation: From KYC to loan disbursement.

-

Multi-document insights: Not just bank statements, but the entire financial profile.

-

Lower operational costs: Lenders cut document processing expenses by up to 40%.

👉 For a glimpse into this future, head over to The Future of Document Processing with AI Agents in Lending.

Frequently Asked Questions

Conclusion: The Smarter Future of Lending

The debate of manual vs automated bank statement analysis isn’t really a debate anymore. While manual reviews may still serve niche cases, the lending industry’s future clearly lies with AI in lending. From faster loan approvals to sharper fraud detection and richer borrower insights, automation gives lenders the edge they need in a competitive market.

And here’s the best part-tools like a modern bank statement analyzer or an integrated bank statement analysis API don’t just save time; they directly impact profitability and customer trust.

The bottom line? Lenders who embrace automation today are the ones writing tomorrow’s success stories