If digital onboarding still means uploading PDFs and waiting for manual verification, it’s not really digital. It’s just digitized paperwork. And in 2025, NBFCs can’t afford that illusion anymore.

Modern borrowers expect speed, trust, and frictionless experiences. The lenders delivering all three aren’t relying on static files – they’re running on real-time data pipelines that connect verification, risk assessment, and credit decisioning within seconds.

That’s the real digital onboarding evolution happening across NBFCs right now.

The Shift: From Document Uploads to Data-Driven Decisions

Traditional onboarding was built around forms and uploads. Every applicant had to submit scanned documents, bank statements, and KYC proofs – followed by long queues for verification.

But here’s what changed:

Over 82% of NBFCs in India (source: RBI Digital Lending Framework Report 2025) are now integrating data-driven onboarding workflows to cut processing time by up to 60%.

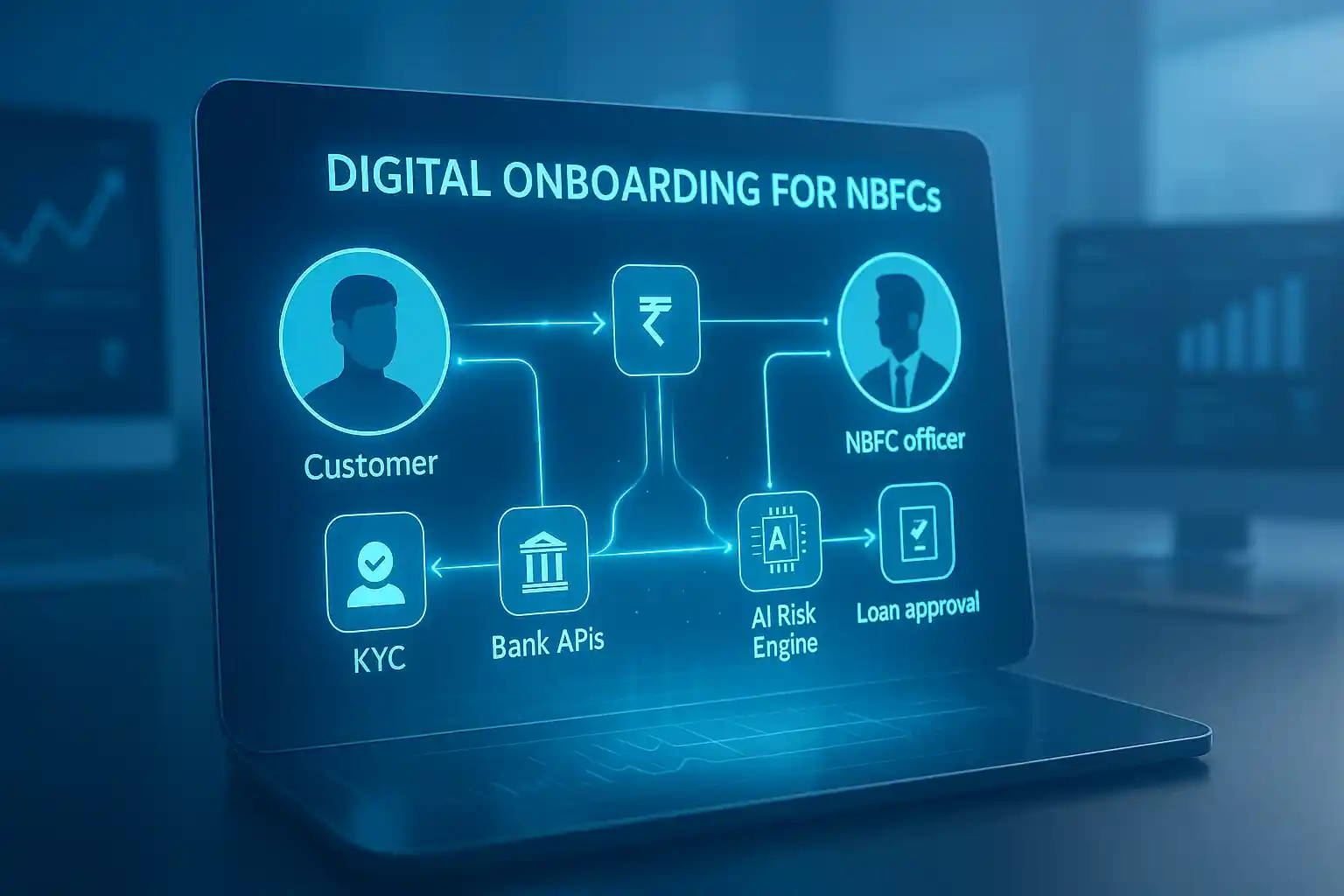

Instead of PDFs, NBFC systems now connect directly to verified data sources:

- Banking APIs for instant transaction data

- CKYC and DigiLocker for identity validation

- GSTN and IT filings for business verification

- Credit bureau and alternate data for behavioral scoring

This live data creates a real-time financial fingerprint of every borrower – updated, accurate, and instantly actionable.

The Real Meaning of Digital Onboarding

Digital onboarding isn’t just an interface upgrade. It’s a process reimagination.

For NBFCs, true digital onboarding means:

- No manual touchpoints. Every step – from KYC to risk scoring – runs on automation.

- Faster turnaround time. Loan approvals happen within minutes, not days.

- Smarter risk detection. Systems flag anomalies through pattern-based intelligence.

- Data consistency. Information flows directly from verified databases – no human errors.

Take a cue from the ideas discussed in NBFC Software Success Stories: Case Studies of Rapid Growth and Digital Transformation – lenders that moved to data-led onboarding reported not just speed, but higher borrower retention and better compliance outcomes.

How Real-Time Data Improves Onboarding Efficiency

Think of traditional onboarding as a snapshot, and real-time onboarding as a live stream.

When an NBFC’s system connects directly to financial data, it gains instant context — understanding income stability, spending behavior, and risk exposure in seconds.

Here’s what this transformation looks like in practice:

- Real-time income validation: Instead of reviewing PDF statements, systems pull 6 months of live bank data via secure APIs.

- Auto KYC match: Digital onboarding platforms verify PAN, Aadhaar, and address in milliseconds.

- Behavioral scoring: AI reads transaction rhythm – salary consistency, EMI history, even investment patterns.

- Fraud prevention: Live data prevents tampering that’s common with uploaded documents.

In short, NBFCs get speed and certainty in the same workflow – something that wasn’t possible a few years ago.

Where Bank Statement Analysis Still Matters

Even in this data-driven setup, bank statement analysis continues to play a key role – just in a smarter way.

Instead of being a slow, manual review task, it now works as an automated engine behind decision-making. Advanced tools – like a bank statement analyser tool for nbfc – turn transaction-level data into meaningful insights such as income volatility, recurring expenses, or hidden liabilities.

This not only supports faster credit scoring but also adds transparency to customer onboarding – a crucial compliance metric under RBI’s Latest NBFC Compliance Framework 2025.

Connecting the Tech Stack: Data Integration as the Backbone

Digital onboarding doesn’t work in isolation. It needs deep integration with the NBFC’s loan origination system (LOS), CRM, and risk engines.

That’s why the smartest lenders are building their systems around unified NBFC software frameworks – as explored in Understanding NBFC Software Features: What Lenders Need in 2025.

By syncing real-time data sources with decision logic, NBFCs eliminate silos, improve data accuracy, and make onboarding scalable across multiple loan products – from personal credit to MSME financing.

Compliance + Automation = Trust

Regulatory bodies are getting sharper about how NBFCs collect and verify data. Manual verification simply can’t keep up.

Real-time onboarding makes compliance automatic:

- KYC and AML checks are performed instantly.

- Every data access is logged and audit-ready.

- Risk alerts are generated in real time.

In Latest NBFC Compliance 2025, regulators emphasize digital traceability and consent-driven verification – exactly what API-based onboarding delivers.

This automation-first approach helps NBFCs build trust through transparency while staying one step ahead of compliance audits.

The Measurable Impact of Digital Onboarding

NBFCs that have fully implemented digital onboarding report results that go beyond convenience:

- Loan disbursal time reduced by up to 70%

- Verification cost down by 40%

- Fraud incidents reduced by 30%

- Customer satisfaction scores up by 55%

For example, one mid-tier NBFC in southern India replaced manual verification with an automated digital onboarding suite. Their average customer approval time dropped from 48 hours to 25 minutes.

That’s not an improvement — that’s a revolution.

What’s Next: Predictive Onboarding and Embedded Finance

The next wave for NBFCs is predictive onboarding — systems that analyze a customer’s data in real time and pre-approve limits even before application submission.

As highlighted in How NBFC Software is Transforming Digital Lending in India (2025 Edition), fintech ecosystems are now embedding these workflows across platforms — from loan apps to accounting dashboards – creating connected lending journeys where customers are verified, scored, and onboarded instantly.

Soon, onboarding won’t be a step – it’ll be a background process happening invisibly, powered entirely by live data.

Final Thought

Digital onboarding isn’t about going paperless anymore – it’s about going effortless.

The NBFCs leading this charge are those that understand one truth: data is the new document.

Every second saved, every click reduced, every data point connected – it all builds toward one goal:

A customer journey that’s instant, intelligent, and incredibly human.