Imagine a small business owner, eager to expand but held back by loan rejection. The reason? Traditional credit appraisal methods failed to capture the true financial health hidden in their complex bank transactions.

What if a smarter, data-driven system could see beyond the surface to offer fair lending? Welcome to the revolution in credit appraisal powered by data analytics.

Credit appraisal, the backbone of responsible lending decisions, is undergoing a transformation. Gone are the days when lenders relied only on static credit scores or paper-heavy manual assessments.

Today, dynamic data analytics—especially bank statement analysis software—brings unprecedented accuracy and fairness to lending.

Understanding Credit Appraisal in the Digital Age

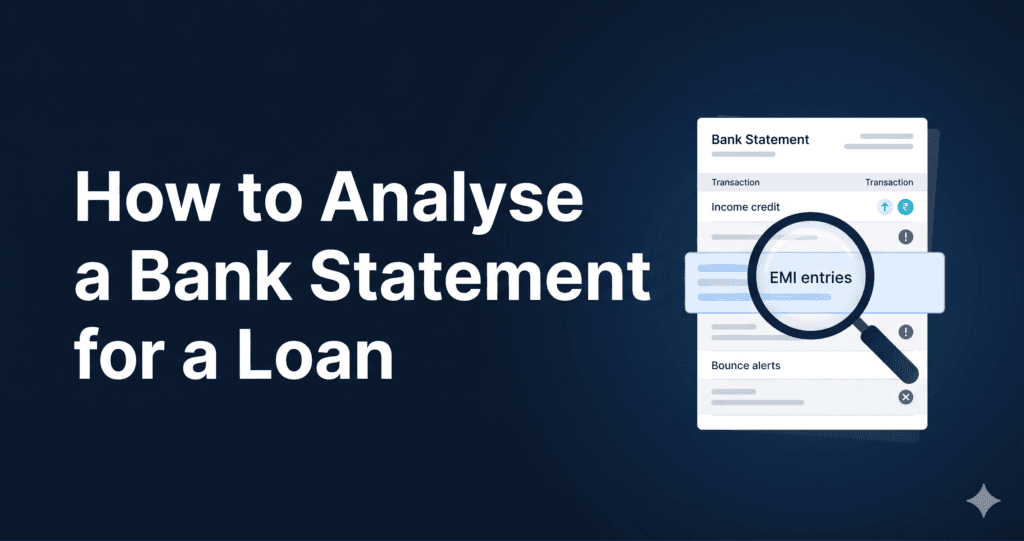

At its core, credit appraisal means assessing a borrower’s ability to repay loans responsibly. Traditionally, this meant reviewing credit history, income statements, and collateral. However, these methods often missed real-time nuances, especially for individuals or businesses with fluctuating incomes or informal financial patterns.

Data analytics changes the game by incorporating the detailed analysis of bank statements. Modern bank statement analysis tools automatically sift through months or years of transactions, flagging income consistency, spending patterns, and financial behavior that simple credit scores overlook.

This analysis of bank statements offers a 360-degree view of the borrower’s financial health.

Why Data Analytics is a Game Changer for Responsible Lending

Lenders face the constant challenge of minimizing risk while avoiding unfair rejections. Data analytics empowers them with:

-

Greater Accuracy: Algorithms assess trends, seasonal variations, and anomalies in bank transactions, providing a realistic cash flow picture.

-

Reduced Bias: Automated analysis limits human error and unconscious bias inherent in manual credit appraisals.

-

Faster Decisions: Automation speeds up the loan approval process without sacrificing rigor.

-

Expanded Access: Borrowers previously marginalized due to lack of formal credit histories can now demonstrate creditworthiness through detailed bank statement analysis.

Take, for example, NBFCs (Non-Banking Financial Companies) that leveraged advanced bank statement analysis software. They reported up to a 30% reduction in non-performing assets due to more precise credit appraisals. Moreover, they expanded credit access to micro-entrepreneurs who had only informal records before—a win-win for inclusive growth.

What Makes a Good Bank Statement Analysis Tool?

To genuinely reinvent credit appraisal, a bank statement analysis tool must do more than just list transactions.

-

Intelligent Categorization: Sorting income, expenses, transfers, and irregular one-offs helps identify true financial trends.

-

Risk Scoring: Assigning risk scores based on transaction patterns and contextual factors improves loan decision accuracy.

-

Customizable Reporting: Tailored insights allow lenders to focus on specific criteria critical to their lending model.

-

Seamless Integration: Compatibility with existing core banking or lending platforms ensures smooth workflows.

Overcoming Common Doubts About Data-Driven Credit Appraisal

Skepticism is natural when new technology redefines established processes. Common concerns include:

-

“Can data analytics truly capture financial risk?” Absolutely. While no system is 100% foolproof, analytics analyze vast data with consistency impossible for manual reviews.

-

“What about data privacy and security?” Modern analysis tools comply with stringent data protection standards, encrypting sensitive information and ensuring lender-borrower confidentiality.

-

“Is this technology only for big banks?” Not at all. Many tailored bank statement analysis tools cater specifically to fintechs, NBFCs, and even auditors looking to enhance credit appraisals.

The Future of Credit Appraisal: Smarter and More Human

Beyond algorithms, data analytics helps lenders spend more time on nuanced, human judgment—understanding contexts like industry-specific cycles or entrepreneurial spirit. The blend of data-driven insights with professional discretion creates a robust, responsible lending environment.

As more lenders adopt bank statement analysis software, borrowers gain confidence through transparency and fairness in credit appraisal. It’s no longer just about crunching numbers but unlocking financial opportunities responsibly.

Conclusion

Credit appraisal has stepped into a new era, where data analytics powers fairness, speed, and inclusivity. The next time you think of lending, imagine a system that reads between the bank statements’ lines to say “Yes” more wisely.

Ready to elevate your lending decisions? Explore how our Bank Statement Analysis Tool can be your secret weapon for smarter credit appraisal and responsible lending. Because fair lending isn’t just good business—it’s the future.

If you want to see this in action, check out Pro analyser’s Bank Statement Analyser and discover how data transforms lending for the better. Lending smarter, not harder, has never been easier!