Lending Using Bank Statements

Bank Statement Analysis for DSAs: How to Pre-Qualify Borrowers Effectively

As lending becomes faster and more data-driven, DSAs are expected to do more than collect documents and forward applications. Lenders increasingly rely on cash-flow-based underwriting, where actual banking behavior carries more weight than declared income. In this environment, Bank Statement Analysis for DSAs has become a foundational step in borrower pre-qualification. It enables DSAs to

Master Your Lending: The 2026 Guide to Bank Statement Analysis for NBFCs

In the fast-paced lending landscape of 2026, speed is the new currency. For Non-Banking Financial Companies (NBFCs), the challenge is no longer just about finding customers, it is about deciding who to trust, and doing it in seconds. Manual reviews are a relic of the past. Relying on a credit score alone is like looking

How to Use Bank Statement Analysis for Loan Approvals for Self-Employed and NTC Borrowers

Loan underwriting was designed for salaried borrowers with predictable income and established credit histories.But lending realities have changed. A large and growing share of applications now comes from self-employed individuals and New-to-Credit (NTC) borrowers. These applicants may run profitable businesses or earn steady income, yet fail traditional checks due to irregular documentation or missing bureau

How Pro Analyser Strengthens Loan Risk Analysis for Lenders

Loan risk analysis has always been the foundation of lending. Every approval, rejection, and pricing decision depends on how accurately a lender can assess risk. Yet, the nature of risk itself has changed. Borrowers today are more diverse. MSMEs, self-employed professionals, gig workers, and digital businesses do not always fit into traditional credit models. Balance

Cash Flow Assessment for Lending: Insights from Bank Statement Analysis

In lending, numbers alone do not tell the full story. Balance sheets can be outdated. Financial ratios can be engineered. Collateral values fluctuate. What consistently reflects a borrower’s true repayment ability is cash flow. That is why cash flow assessment has become central to modern credit underwriting. Instead of relying solely on static financials, lenders

How to Automate Credit Risk Analysis Using a Financial Statement Parser

Credit risk analysis sits at the heart of every lending decision. Yet, many finance teams still depend on manual reviews of PDFs and spreadsheets to assess borrower risk. This approach is slow, difficult to scale, and increasingly misaligned with today’s data-driven lending environment. As underwriting volumes rise and decision timelines shrink, automation has become essential.

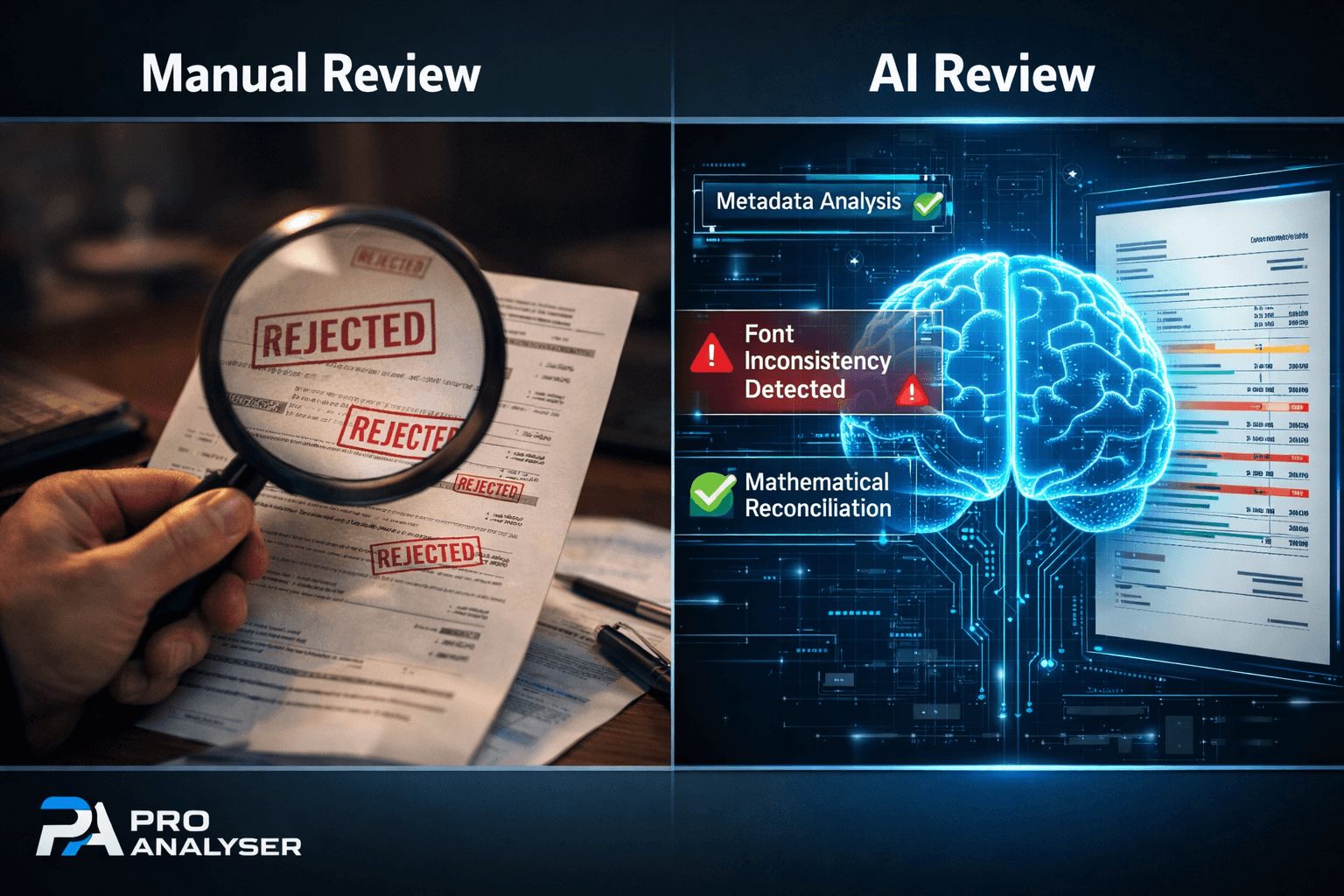

5 Ways AI Detects Tampered Bank Statements that Manual Review Misses

In the high-stakes world of lending and auditing, a bank statement is more than just a list of transactions, it is the ultimate proof of a borrower’s financial health. However, as digital editing tools become more sophisticated, “doctoring” these documents has become alarmingly easy. For years, credit officers relied on manual “sight checks” to spot

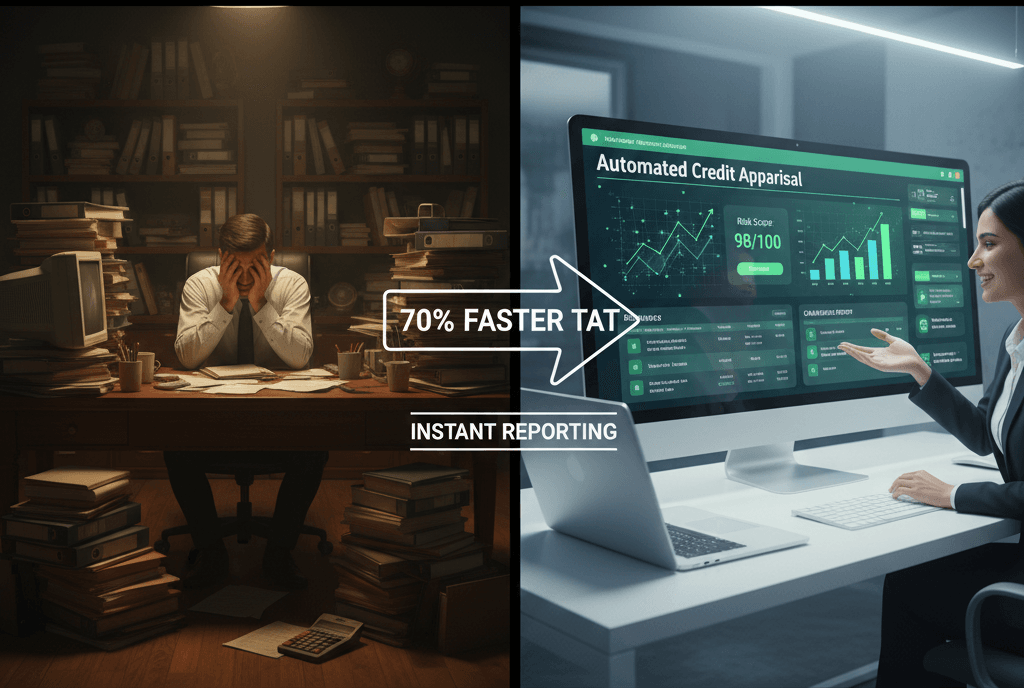

Stop Losing Borrowers: How Automated Credit Appraisal Slashes Loan TAT by 70%

In the competitive world of lending, speed isn’t just an advantage – it’s a survival requirement. Today’s borrowers, from retail individuals to seasoned MSME entrepreneurs, value time as much as interest rates. If your Loan Turnaround Time (TAT) is measured in weeks while your competitor’s is measured in hours, you aren’t just slow; you’re losing

Decoding Modern Bank Statement Terms

Ever stared at your bank statement and felt like it was quietly daring you to decode it? You’re definitely not alone. Most professionals skim through it confidently… until a strange entry like “REV-IMPS-UTR-XXXX” appears and suddenly your pulse jumps just a bit. That’s exactly why this guide steps in – to simplify confusing bank statement

Explainable AI in Lending: The Rise of Integrated Financial Intelligence for Transparent Credit Decisions

Lending is getting a conscience – and it starts with clarity. For decades, credit systems worked like locked vaults. A loan would be approved or rejected, but borrowers rarely knew why. Even relationship managers struggled to explain how the algorithm weighed one factor against another. As digital lending exploded, this lack of visibility became a