Have you ever wondered why your tech-savvy friend got an instant loan approval on his phone, while another was asked to dig up three years’ worth of salary slips and utility bills—just for a modest personal loan? Welcome to the new era of retail lending, where Artificial Intelligence (AI) is the star underwriter, and its decisions are as swift as your UPI transactions.

Gone are the days of one-size-fits-all risk checks and endless manual document verifications. Let’s open up the curtain and see how AI is giving retail loan underwriting a major glow-up.

The Brave New World of AI-Powered Risk Scoring

Forget the old “CIBIL Score only” mantra. Modern lenders are hungry for more signals, and AI models oblige—chewing through your bank transactions, e-commerce splurges, GST filings, and even your mobile recharges. For India’s 400 million “thin-file” or new-to-credit citizens, this means access where there was none.

Example: A Kirana store owner, with no formal loan history, gets approved for working capital because AI spots steady UPI sales and regular digital utility payments.

Talk Less, Scan More: Automated Document Checks

Who wants to shuffle through a pile of paperwork at a branch? Not your customer, and definitely not your ops team! AI-powered OCR (Optical Character Recognition) and Natural Language Processing (NLP) now scan, verify, and extract details from payslips, bank statements, and IDs—no human fatigue, no “oops, we missed page 3.”

- Average document verification time has dropped from days to under 5 minutes at leading fintech. (AI in Loan Underwriting)

- OCR accuracy rates in Indian lending touch up to 98% on clear scans.

Beyond Income Slips: Real-Time Employment and Income Verification

Still calling HR for verifying employment? AI now checks public data, social profiles, payroll APIs, and those neat monthly salary credits to confirm who’s paying your applicant—and how much. Manual verification teams are rapidly being re-skilled (or retired).

Example: A gig worker’s loan is approved based on monthly bank credits from multiple platforms, flagged and summarized by automated bank statement analysis software.

The Sherlock Holmes of Fraud Detection

Think forgery is cleverer than a machine? Guess again. AI finds mismatched addresses, duplicate PANs, and abnormal sequence patterns (like five applications from the same IP, in four minutes). Lending fraud rates have gone down by as much as 40%, thanks to these eagle-eyed algorithms.

Mini Table: AI Risk Checks vs. Traditional Checks

| AI Power | Old School | |

| Doc Checks | Seconds | Hours/Days |

| Income Proof | API/Banks | Manual Call/Docs |

| Fraud Flags | Real Time | Often Missed |

| Credit Scoring | Dynamic, Uses 100+ Signals | Bureau Only |

Dynamic Offers: Bye-Bye, Boring Loan Products

“One-rate-fits-all” is so 2015. Today’s AI models create personalized offers—dynamic loan amounts, terms, and flexible EMIs—calculated on the fly. Got a low but steadily rising bank balance? You might get a better deal than a high-flying but volatile spender.

Stats: Over 60% of new fintech loans in India are now offered with AI-powered dynamic pricing. (vymo)

Continuous Portfolio Monitoring: Not Just a ‘Yes’ or ‘No’

Approval isn’t the endgame. AI tools now monitor borrower behavior post-disbursal—checking payment trends, spending signals, and even late-night UPI sprees—to catch stress signals. Early alerts lower lender NPAs and give you a chance to help customers before they slip.

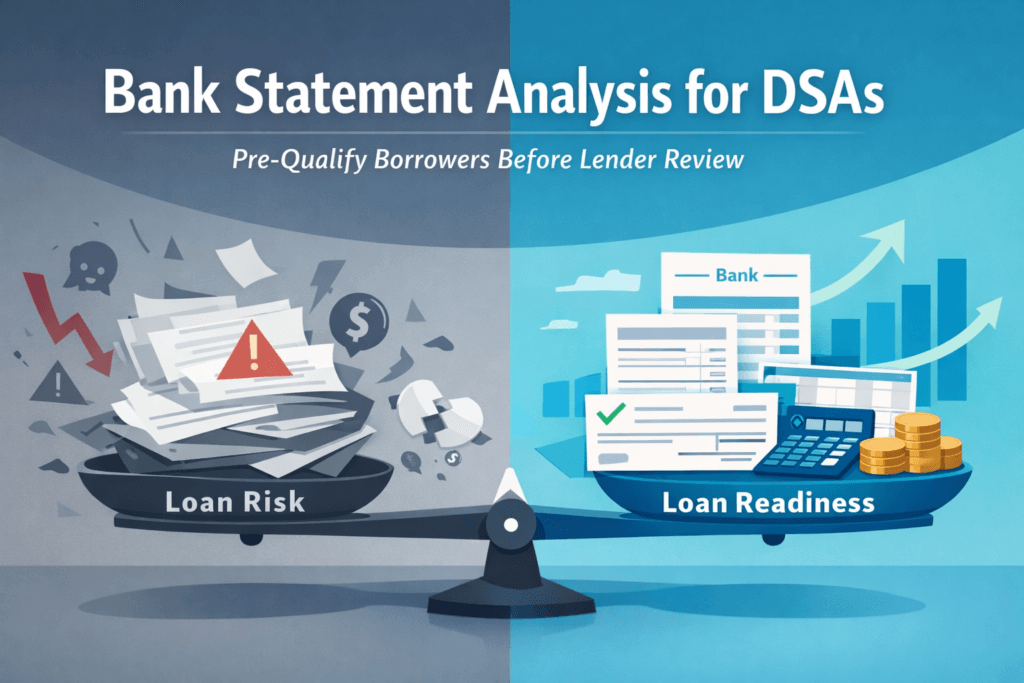

Solution highlight: That’s where using a robust bank statement analysis tool streamlines portfolio health checks and strengthens early warning signals—no matter your loan volume.

The Rise of Explainable AI

“Computer says no” isn’t good enough for regulators—or applicants. Modern AI systems now tell you why a loan was declined (maybe it was those three bounced cheques), or break down what tipped a decision into the green zone. Goodbye, opaque black-box decisions; hello, transparency.

Summing Up (With Less Headache, More Headroom)

AI has ushered in a golden age for retail loan underwriting—making loan approvals fairer, faster, and ridiculously efficient. Whether you’re a traditional lender, NBFC innovator, or a sharp-eyed auditor, the tools you embrace now—like cutting-edge bank statement analysis software—will shape tomorrow’s profits, portfolio hygiene, and customer delight.

Ready to toss out slow, manual checks for some brainy automation? Explore how our bank statement analysis tool can simplify credit risk like never before—and let your next underwriter be an algorithm that doesn’t even take tea breaks.

Curious how these AI superpowers can boost your own lending game? Dive into our bank statement analysis software today—because the future of lending doesn’t wait!