For years, lenders have relied on income statements to judge repayment capacity. Yet defaults persist—even among borrowers with stable, high salaries. Income shows earning power, not financial discipline. The real indicator of repayment reliability is cash-flow stability, not static income data.

This is where the Volatility Score transforms credit assessment. It provides a sharper, data-driven view of repayment risk—by measuring how consistently money flows in and out, not just how much is earned.

What Is a Volatility Score?

A Volatility Score quantifies the stability of an individual’s cash flow over time. It analyses bank transactions—credits, debits, and balance patterns—to assess how predictably money moves through an account. Unlike a one-time income proof, it captures living financial behaviour:

- Are credits regular or irregular?

- Are balances healthy or frequently low?

- Are expenses controlled or erratic?

Modern lending platforms integrate this score into their risk models. Each applicant receives a score from 0 to 1—where lower values represent stable, disciplined financial management, and higher values signal erratic cash flow.

This single number helps lenders instantly gauge whether a borrower can reliably manage monthly EMIs.

How to Calculate a Volatility Score

The Volatility Score measures the consistency of net monthly cash flow—the difference between total inflows and outflows—over the last 6 to 12 months.

Lenders review bank transactions to identify:

-

Average Monthly Net Cash Flow – the typical monthly surplus.

-

Standard Deviation – how much the monthly figures vary.

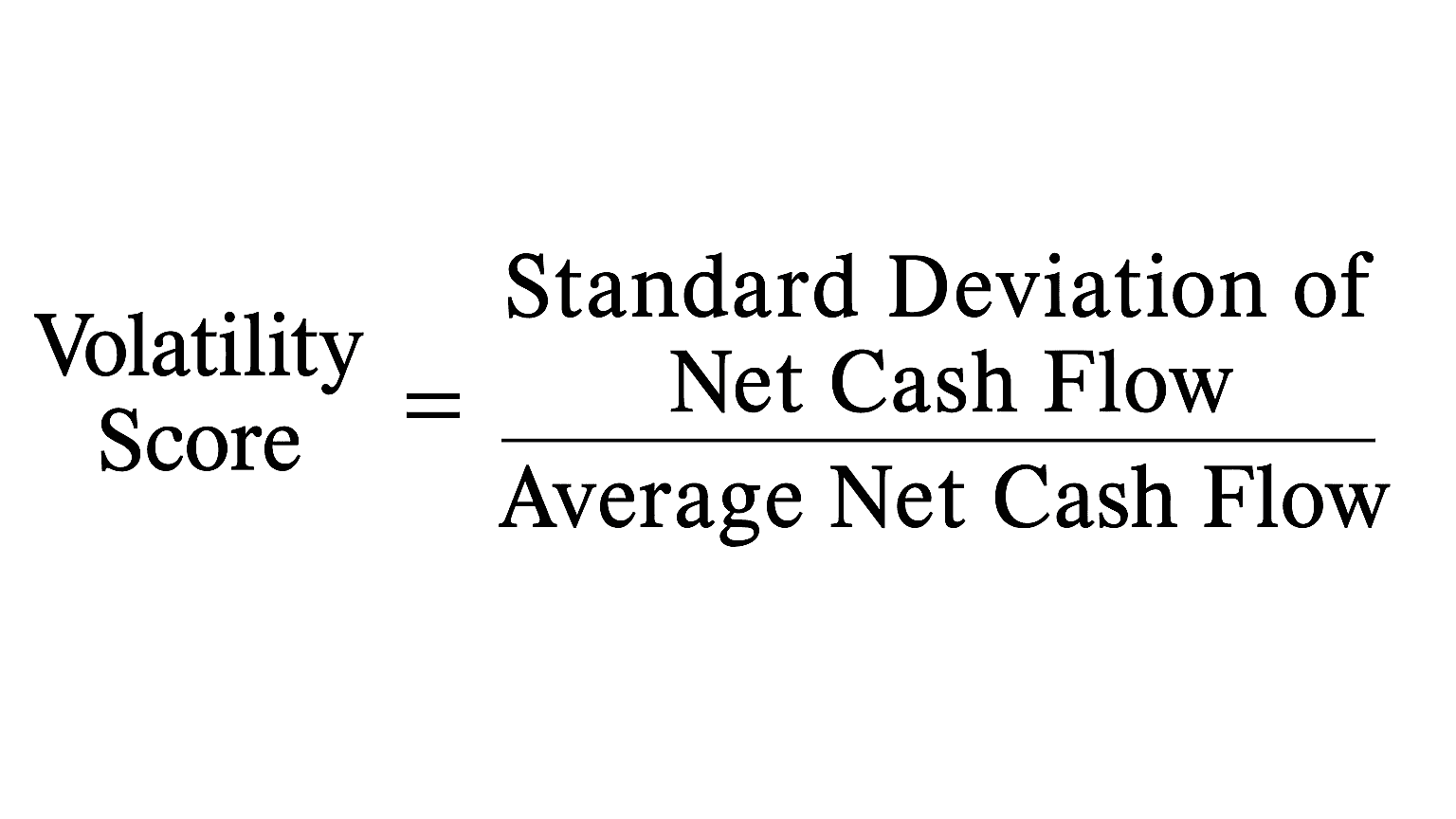

The formula is simple:

A higher score indicates unstable finances and greater lending risk. A lower score signals consistent inflows and prudent spending.

With Pro Analyser, this entire calculation is automated. Lenders can process bank statements in minutes and receive actionable insights—offering a real-time snapshot of financial predictability that income data alone cannot provide.

Why Cash-Flow Volatility Predicts Repayment Better

Volatility is the true stress test of a borrower’s stability. It reflects how someone’s finances behave under real-life variability—something income statements overlook.

Imagine two borrowers. One is a freelancer earning between ₹20,000 and ₹1,00,000 per month. The other earns a fixed ₹50,000. The freelancer’s average income seems higher, but the inconsistency increases the risk of missing EMIs during lean months.

Data supports this. The RBI Financial Stability Report (June 2024) notes that personal loans sourced from variable or unsecured income segments show default rates near 3.6%, versus 2.3% across the broader banking sector. Among small-ticket borrowers—those with irregular earnings—defaults can exceed 11%.

The Pro Analyser Volatility Score directly addresses this challenge. Its proprietary algorithm evaluates inflows, outflows, recurring transactions, and balance patterns—flagging unstable accounts before they translate into defaults.

By quantifying cash-flow fluctuations, Pro Analyser helps lenders:

- Distinguish consistent earners from volatile ones

- Price risk accurately

- Reduce early-stage delinquencies and protect portfolio quality

Volatility scoring moves credit risk assessment from subjective judgment to evidence-based prediction.

How NBFCs and DSAs Benefit from Volatility Scoring

NBFCs and DSAs are increasingly embedding volatility scoring into their lending workflows. By analysing real bank transactions instead of relying only on income documents or bureau data, they gain a clear, behavioural view of financial discipline.

1. Detect Risk Early

A borrower may show high income yet struggle with uneven cash flow. The Pro Analyser Volatility Score highlights such instability early, helping lenders adjust pricing or decline high-risk cases.

For instance, a DSA using Pro Analyser’s AI engine cut its application review time from nearly two hours to 30 minutes—as the system automatically scored volatility and flagged risky applicants.

2. Approve the Right Borrowers Faster

Gig workers, small business owners, and freelancers are often rejected under traditional models despite disciplined money management. Volatility scoring recognises this stability, allowing lenders to confidently approve financially sound applicants with modest but consistent inflows.

3. Expand Credit Without Increasing Risk

Cash-flow intelligence lets NBFCs and DSAs grow portfolios safely. Institutions using Pro Analyser’s Volatility Score have recorded sharper underwriting precision and lower delinquency rates, particularly in MSME and small-ticket personal loan segments.

Volatility scoring enables lenders to balance growth with control—expanding reach while maintaining risk discipline.

How to Incorporate Volatility Scoring into Credit Decisions

Implementing volatility analysis is simple with Pro Analyser, which integrates seamlessly through a dashboard or API.

1. Automated Bank Statement Analysis

The Pro Analyser Bank Statement Analyser scans 6–12 months of financial data within minutes. It extracts behavioural indicators and produces both an overall credit score and a dedicated Volatility Score.

2. Use Scores to Refine Decisions

-

0.00–0.30 (Low Volatility): Highly stable cash flows; strong repayment reliability.

-

0.31–0.60 (Moderate Volatility): Manageable fluctuations; suitable for standard terms with minor risk adjustments.

-

0.61–1.00 (High Volatility): Frequent income gaps or erratic spending; higher risk requiring collateral or adjusted pricing.

3. Combine with Other Credit Metrics

The Volatility Score complements, not replaces, traditional metrics. When combined with income level, DTI ratio, credit history, and business context, it adds a real-time stability dimension to underwriting.

4. Enable Early Risk Monitoring

Pro Analyser continuously tracks changes in a borrower’s cash flow. A rising score signals instability—irregular deposits, declining balances, or sudden expense spikes—allowing credit teams to act before repayment issues occur.

5. Integrate via Dashboard or API

-

Dashboard: Upload statements directly to the Pro Analyser Platform for instant scoring.

-

API Integration: Embed Pro Analyser into your LOS or CRM for real-time, automated volatility analysis.

-

Custom Rules: Set thresholds (e.g., flag scores above 0.7) to automate underwriting and risk alerts.

Final Thoughts

Traditional credit assessments were built for a different era—when income was predictable and employment steady. Today’s borrowers operate in a dynamic, multi-source income ecosystem. To lend intelligently, institutions must assess financial stability in motion, not just reported income.

The Pro Analyser Volatility Score provides that edge. It empowers lenders with real-time visibility into cash-flow behaviour, enabling faster approvals, smarter pricing, and early risk intervention.

NBFCs, DSAs, and digital lenders using Pro Analyser are already achieving measurable gains in accuracy, efficiency, and portfolio performance.

If your goal is to expand credit safely and strengthen underwriting discipline—

start predicting defaults before they happen.

Book a live demo of Pro Analyser’s Financial Data Analysis Tools.