Credit Risk Assessment

Beyond the Paystub: Why Gig Worker Verification is the Future of Lending

The workforce is shifting rapidly, but traditional credit underwriting often feels stuck in the era of the 9-to-5 desk job. While millions of people now earn high incomes through platforms like Swiggy, Zomato, and Uber, they are frequently rejected by traditional lenders. Why? Because their “paystubs” look like a chaotic stream of micro-transactions rather than

Beyond the Balance: SME Lending Secrets Hidden in Your Bank Statements

Most SME owners view their bank statements as a historical record—a simple trail of where the money went. Lenders, however, see them as a crystal ball. When you apply for SME lending, the credit analyst isn’t just looking at your total revenue. They are reading between the lines to find the “narrative” of your business.

Reducing TAT in SME Lending: The Power of Automated Bank Statement Analysis

The New Era of Credit Assessment for Lenders In the fast-moving world of SME lending, relying only on a credit score is no longer enough. For underwriters and NBFCs, the real truth about a borrower’s health is hidden inside their bank transactions. A deep bank statement analysis allows lenders to see the actual cash flow

Bank Statement Analysis for Fintech Lending: Best Practices 2026

The fintech lending landscape is evolving at an unprecedented pace, and at the heart of this transformation lies a critical capability: bank statement analysis. As fintech companies and traditional lenders compete to capture market share, the ability to accurately interpret financial data has become a competitive differentiator. In 2026, sophisticated bank statement analysis has moved

How DSAs Can Use Bank Statement Analysis to Improve Conversion Rates

Direct Selling Agents (DSAs) face immense pressure to convert leads into successful loan approvals. With average DSA conversion rates hovering around 15-25%, there’s enormous untapped potential. The secret weapon? Bank statement analysis. Modern bank statement analyser tools are transforming how DSAs approach loan applications, turning tedious manual processes into streamlined workflows. By leveraging advanced bank

How to Analyse Cash Deposits in Bank Statements for MSME Lending

For Micro, Small, and Medium Enterprises (MSMEs) in India, cash remains king. From neighborhood kirana stores to local manufacturers, millions of businesses still operate predominantly in cash. For lenders, this presents a unique challenge: how do you accurately assess creditworthiness when a significant portion of income arrives as cash deposits in bank statements? Cash deposit

How to Detect Circular Transactions in Bank Statements: A Guide for NBFCs

In India’s rapidly evolving digital lending ecosystem, Non-Banking Financial Companies (NBFCs) face a sophisticated threat: circular transactions. These orchestrated money flows create the illusion of legitimate business activity or income, deceiving underwriters and artificially inflating creditworthiness. Unlike simple document tampering, circular transactions involve real money movements making them extremely difficult to identify through manual verification.

From Reactive to Predictive: How Automated Analysis Drives NPA Reduction in 2026

In the competitive lending landscape of 2026, the margin for error has vanished. While digital lending volumes are at an all-time high, the challenge of maintaining asset quality remains the top priority for Banks and NBFCs. The secret to sustainable growth isn’t just lending more. it’s lending smarter. The most effective strategy for NPA reduction

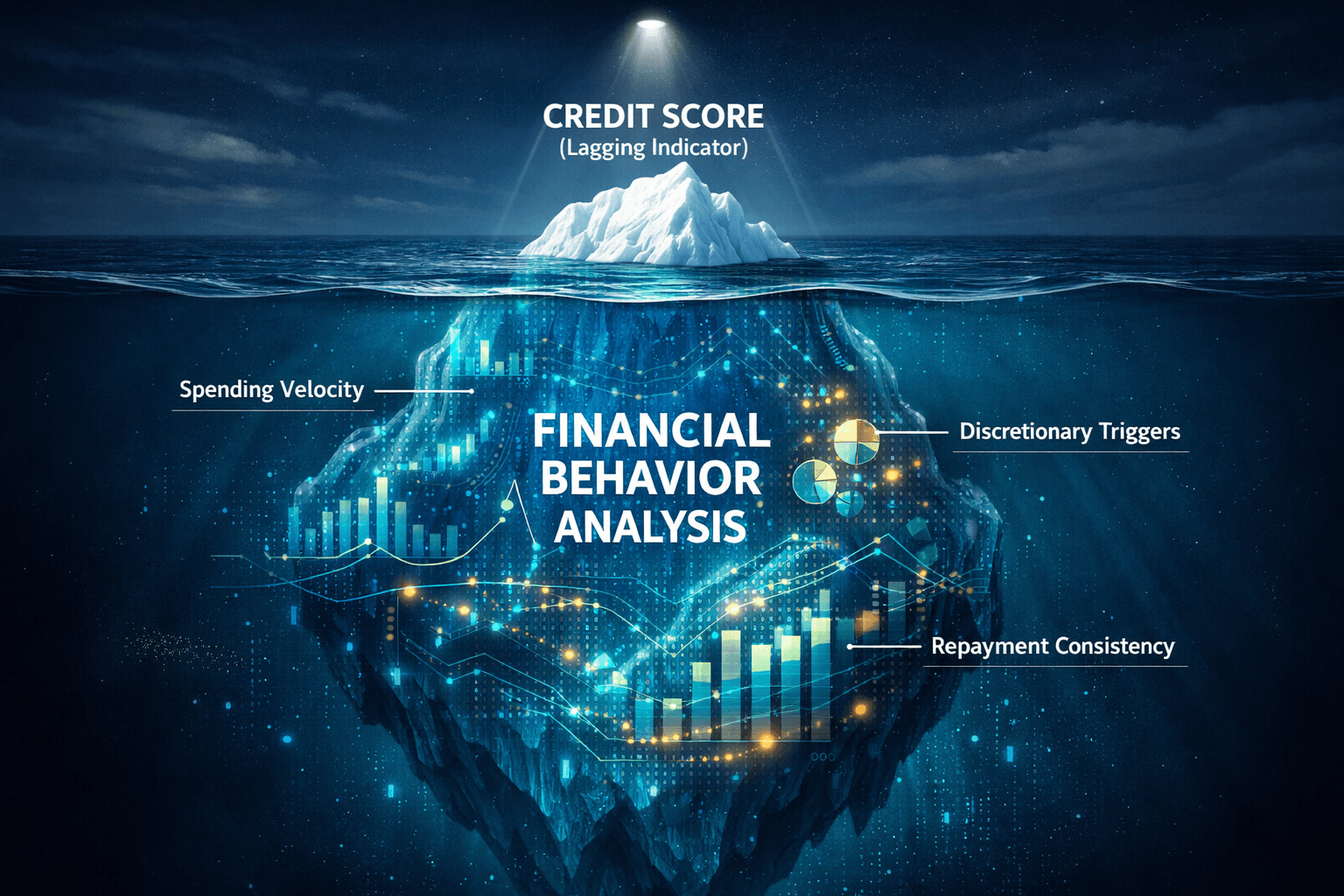

Beyond the Credit Score: Why Financial Behaviour Analysis is the Future of Lending

In the modern lending landscape, a credit score is a lagging indicator. It tells you what happened months ago, but it rarely predicts what will happen tomorrow. To gain a true competitive edge, financial institutions and fintechs are shifting their focus toward Financial Behaviour Analysis. While traditional metrics provide a snapshot of the past, understanding

Optimizing Credit Underwriting: The Strategic Role of Bank Account Analysis in NBFCs

In the high-stakes world of lending, speed is a competitive advantage, but accuracy is a survival requirement. For NBFCs (Non-Banking Financial Companies), the bridge between receiving a loan application and disbursing funds is Bank Account Analysis. Traditionally, this process was a manual hurdle, underwriters spending hours scrolling through hundreds of pages of PDFs. Today, that