Bank Statement analysis

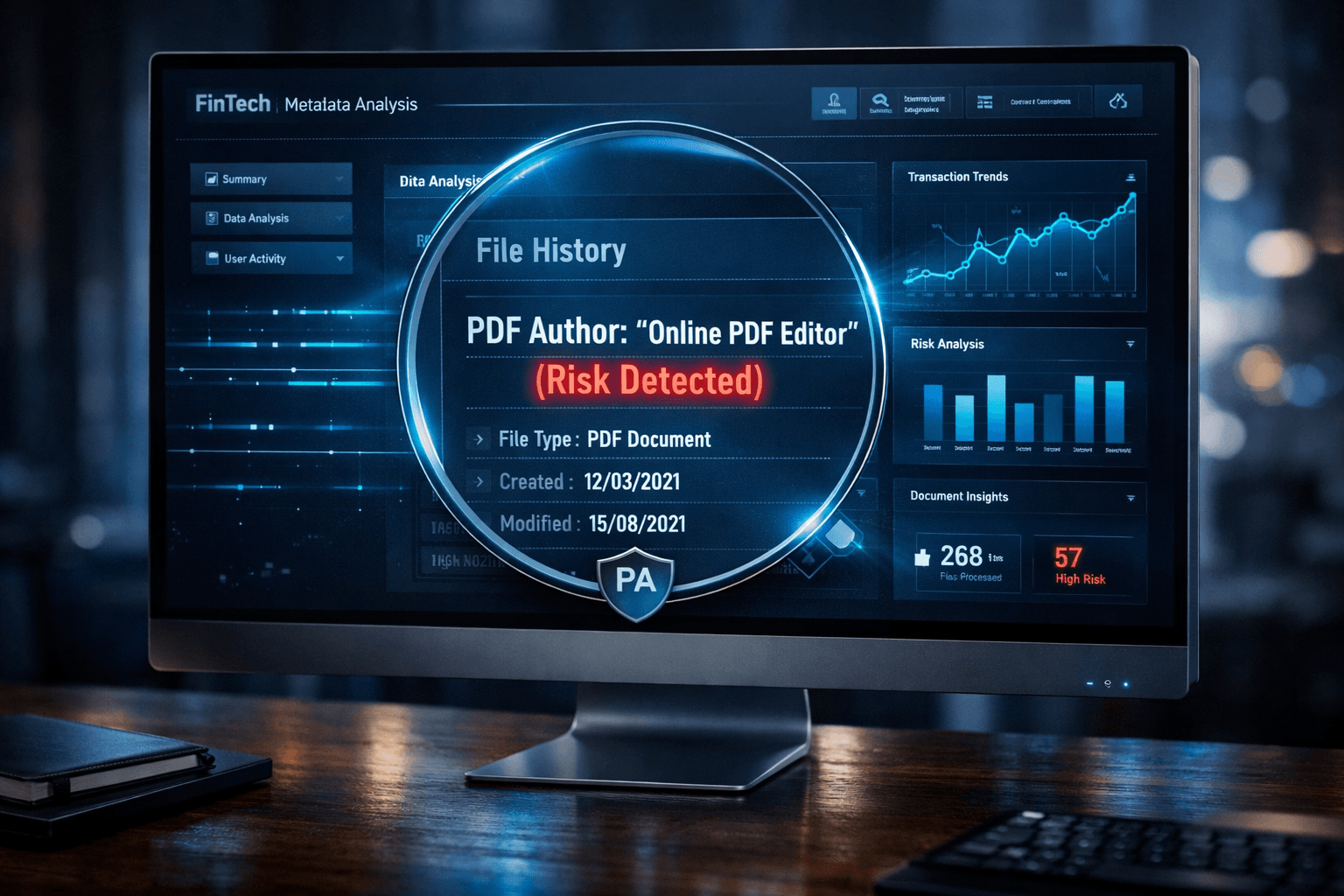

Statement Fraud Detection: Protect Your Lending Business

In the digital lending era, the greatest threat to an NBFC’s loan book isn’t just a “bad” borrower, it’s a “fake” one. As document editing tools become more sophisticated, manual statement fraud detection has become a game of cat and mouse that humans are no longer equipped to win. For modern lenders, the ability to

Optimizing Credit Underwriting: The Strategic Role of Bank Account Analysis in NBFCs

In the high-stakes world of lending, speed is a competitive advantage, but accuracy is a survival requirement. For NBFCs (Non-Banking Financial Companies), the bridge between receiving a loan application and disbursing funds is Bank Account Analysis. Traditionally, this process was a manual hurdle, underwriters spending hours scrolling through hundreds of pages of PDFs. Today, that

Bank Statement Analysis for DSAs: How to Pre-Qualify Borrowers Effectively

As lending becomes faster and more data-driven, DSAs are expected to do more than collect documents and forward applications. Lenders increasingly rely on cash-flow-based underwriting, where actual banking behavior carries more weight than declared income. In this environment, Bank Statement Analysis for DSAs has become a foundational step in borrower pre-qualification. It enables DSAs to

Master Your Lending: The 2026 Guide to Bank Statement Analysis for NBFCs

In the fast-paced lending landscape of 2026, speed is the new currency. For Non-Banking Financial Companies (NBFCs), the challenge is no longer just about finding customers, it is about deciding who to trust, and doing it in seconds. Manual reviews are a relic of the past. Relying on a credit score alone is like looking

How to Use Bank Statement Analysis for Loan Approvals for Self-Employed and NTC Borrowers

Loan underwriting was designed for salaried borrowers with predictable income and established credit histories.But lending realities have changed. A large and growing share of applications now comes from self-employed individuals and New-to-Credit (NTC) borrowers. These applicants may run profitable businesses or earn steady income, yet fail traditional checks due to irregular documentation or missing bureau

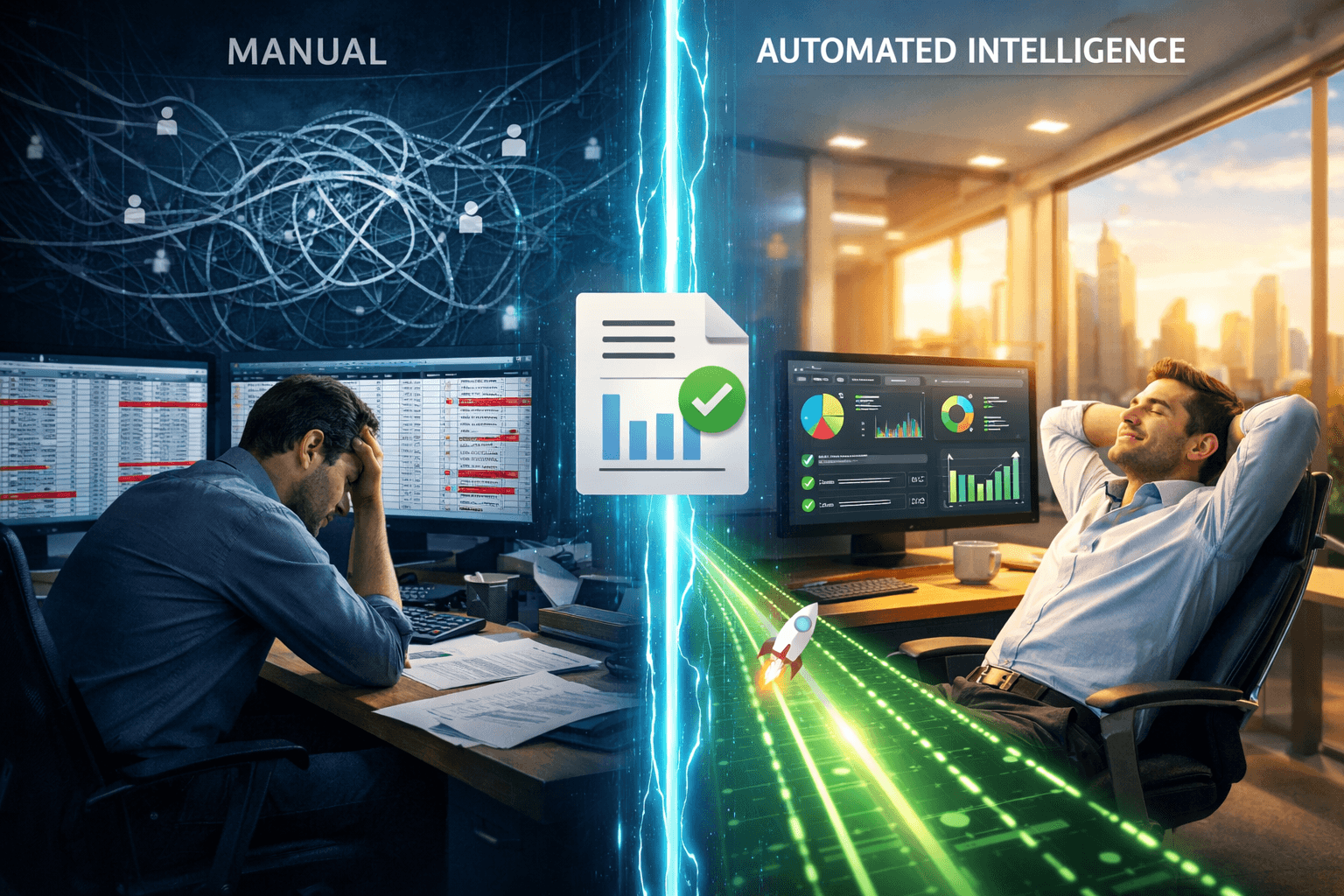

The Hidden Cost of “Manual Analysis”: Why Automated Transaction Categorization is a Must for Scaling FinTechs

If you’ve ever sat staring at a spreadsheet at 6:00 PM, trying to figure out if SQ *PURCHASE_332 was a legitimate business expense or a coffee run, you know the specific kind of headache I’m talking about. For years, we’ve accepted “manual data entry” as just part of the job in finance and lending. We

How Pro Analyser Strengthens Loan Risk Analysis for Lenders

Loan risk analysis has always been the foundation of lending. Every approval, rejection, and pricing decision depends on how accurately a lender can assess risk. Yet, the nature of risk itself has changed. Borrowers today are more diverse. MSMEs, self-employed professionals, gig workers, and digital businesses do not always fit into traditional credit models. Balance

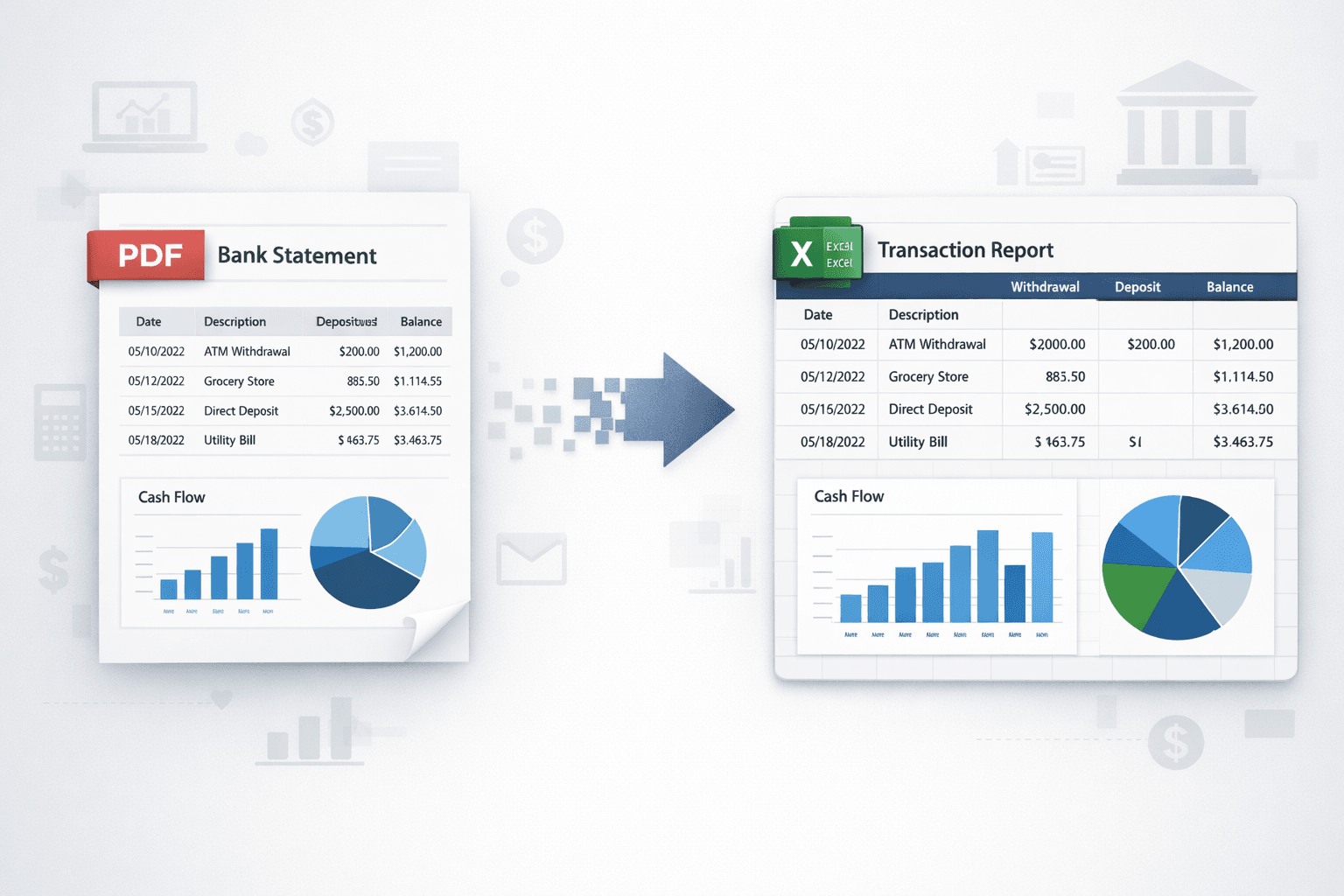

How to Convert PDF Bank Statements to Excel for Accurate Analysis

Bank statements are one of the most reliable indicators of real financial behavior. They capture actual cash movement, spending discipline, and income stability. Yet, despite their importance, bank statements are still commonly shared as PDFs of static files that are not built for analysis. For finance professionals, this creates a recurring challenge. You cannot build

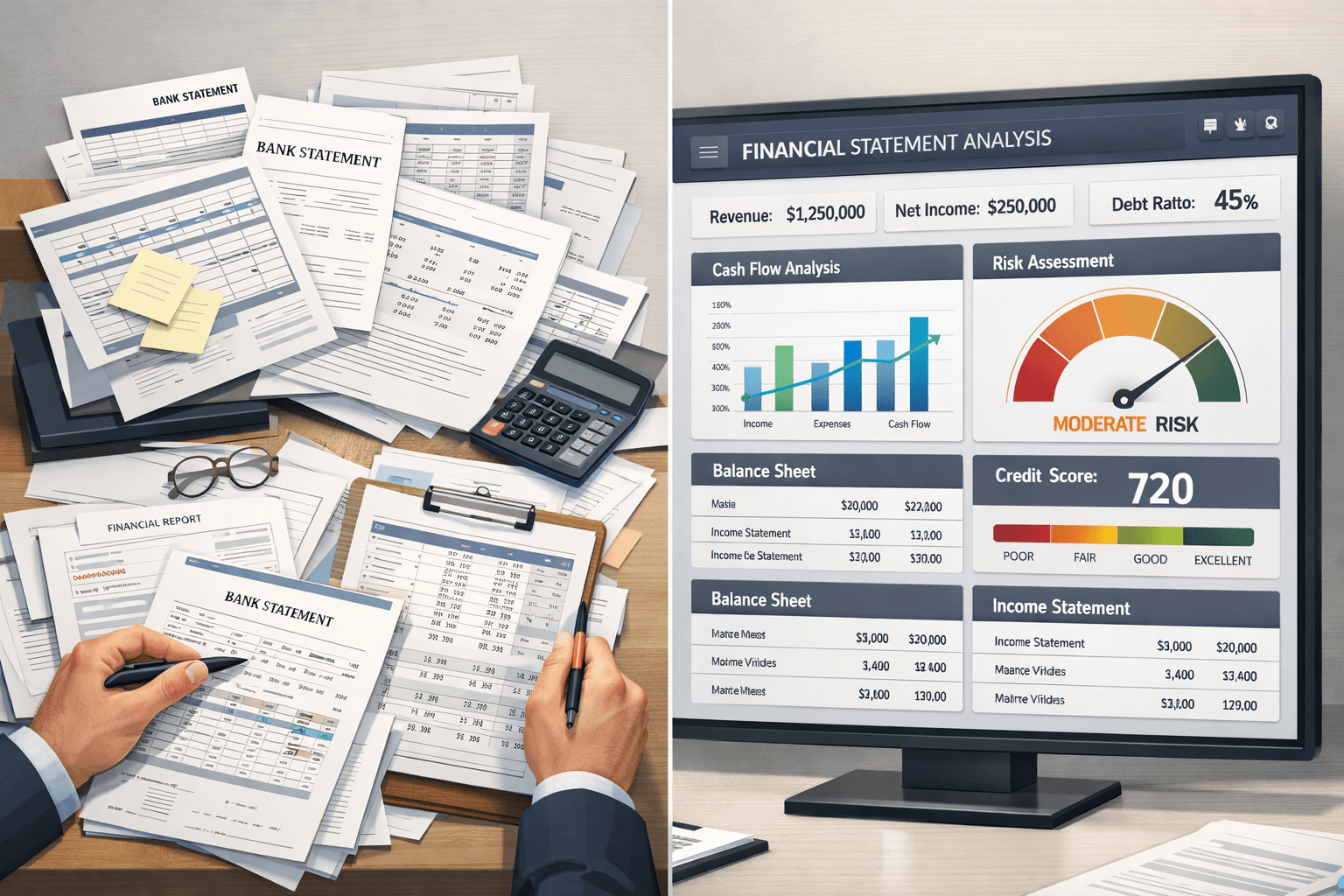

How to Automate Credit Risk Analysis Using a Financial Statement Parser

Credit risk analysis sits at the heart of every lending decision. Yet, many finance teams still depend on manual reviews of PDFs and spreadsheets to assess borrower risk. This approach is slow, difficult to scale, and increasingly misaligned with today’s data-driven lending environment. As underwriting volumes rise and decision timelines shrink, automation has become essential.

Why Many NBFCs Prefer Pro Analyser Over Full-Suite Platforms

NBFCs today are operating under more pressure than ever: larger loan volumes, tighter risk controls, and rising fraud attempts. In this environment, technology is no longer optional — it’s a major factor in portfolio quality.This is why many lenders are shifting away from heavy, multi-module systems and choosing focused tools built specifically to improve credit