Blog

The “Perfect Borrower” Trap: Catching Hidden Loans with Bank Statement Analysis

Catching hidden loans before they become NPAs is one of the biggest challenges in modern credit underwriting. Imagine this: You have an application from a seemingly perfect borrower — high income, good job stability, and a decent credit score according to the major bureaus. You approve the loan based on your standard eligibility assessment. Three

Salary vs Business Income: How to Categorize Mixed-Income Profiles for Smarter Lending

The borrower who earns well – but confuses every underwriting model The application arrives. Monthly credits look healthy. The number is there. But when your team runs it through a bank statement analyser, the picture fragments — some credits are salary, some are business transfers, some are client payments, and one month shows a large

EMI Analysis for Lenders: Use the EMI Burden Ratio to Stop Bad Loans Before They Start

The loan that looked safe – until it wasn’t The file looked clean. Stable employer. Salary credited on time every month. A CIBIL score sitting comfortably above 750. Your team approved the loan. Six months later, the borrower missed two EMIs. Sound familiar? In most cases, the warning was there — buried inside the bank

How to Analyse a Bank Statement for a Loan: A Step-by-Step Guide for NBFCs & DSAs

Every loan application tells a story. And the clearest version of that story is written in the applicant’s bank statement. For NBFCs and DSAs, knowing how to analyse a bank statement for a loan is one of the most critical skills in the lending process. Done right, it reveals income patterns, existing obligations, and financial

Predictive Cash Flow Analysis: Turning Historical Data Into Future Growth

Most finance teams manage cash flow by looking through a rear-view mirror. You track what was spent, reconcile what came in, and hope the delta remains positive. But in a volatile market, looking backward isn’t enough. True financial leadership requires a windshield. Transitioning from static tracking to cash flow forecasting allows you to move from

Beyond the Paystub: Why Gig Worker Verification is the Future of Lending

The workforce is shifting rapidly, but traditional credit underwriting often feels stuck in the era of the 9-to-5 desk job. While millions of people now earn high incomes through platforms like Swiggy, Zomato, and Uber, they are frequently rejected by traditional lenders. Why? Because their “paystubs” look like a chaotic stream of micro-transactions rather than

Beyond the Balance: SME Lending Secrets Hidden in Your Bank Statements

Most SME owners view their bank statements as a historical record—a simple trail of where the money went. Lenders, however, see them as a crystal ball. When you apply for SME lending, the credit analyst isn’t just looking at your total revenue. They are reading between the lines to find the “narrative” of your business.

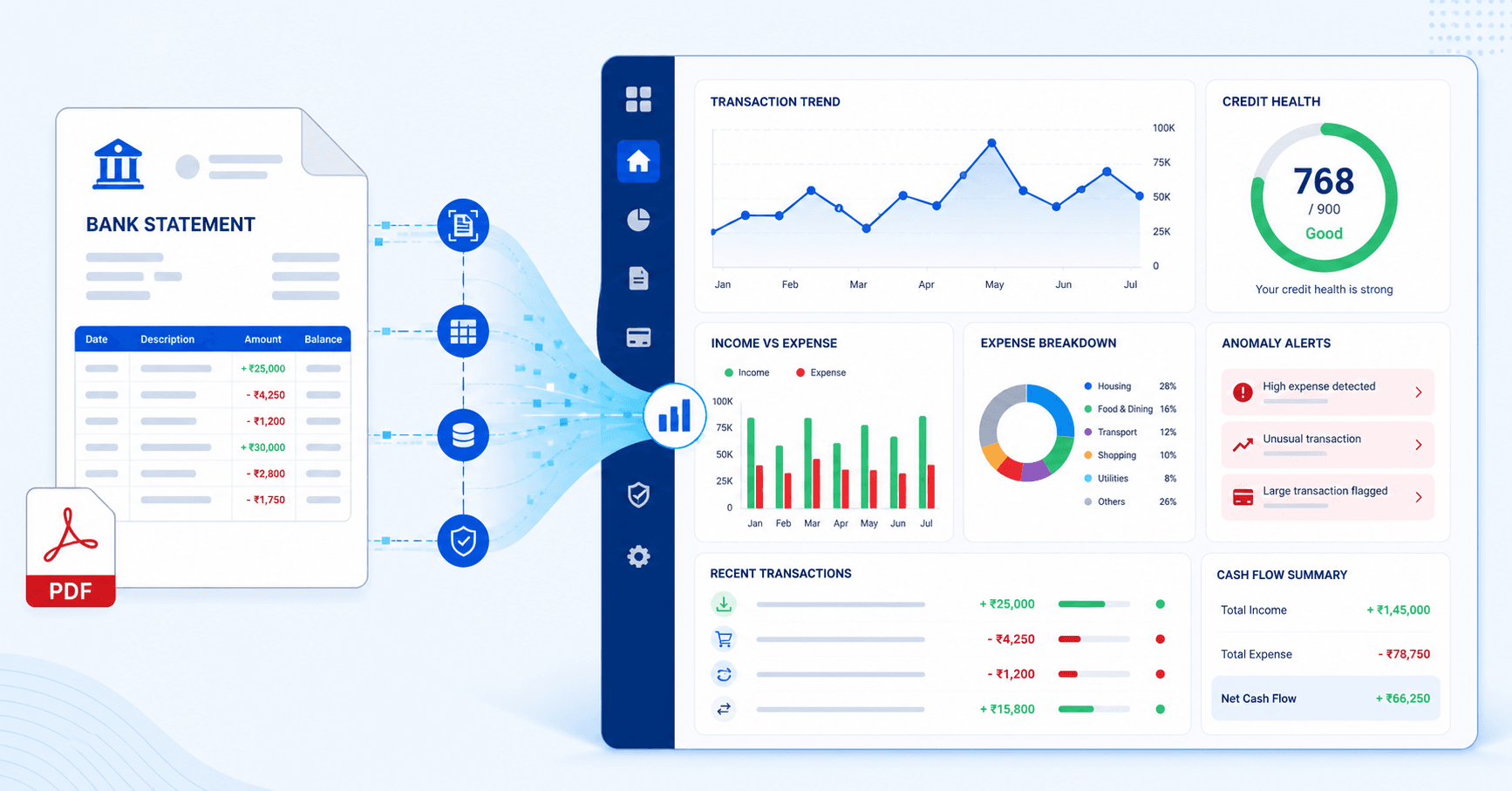

The Complete Guide to Bank Statement Analysis: What It Is and Why It Matters

In today’s fast-paced lending environment, knowing how to analyse bank statements is no longer optional — it is a core competency for every NBFC, lender, and credit professional. Whether you are processing retail loans, MSME credit, or personal finance products, the bank statement tells a story that no other document can. It reveals a borrower’s

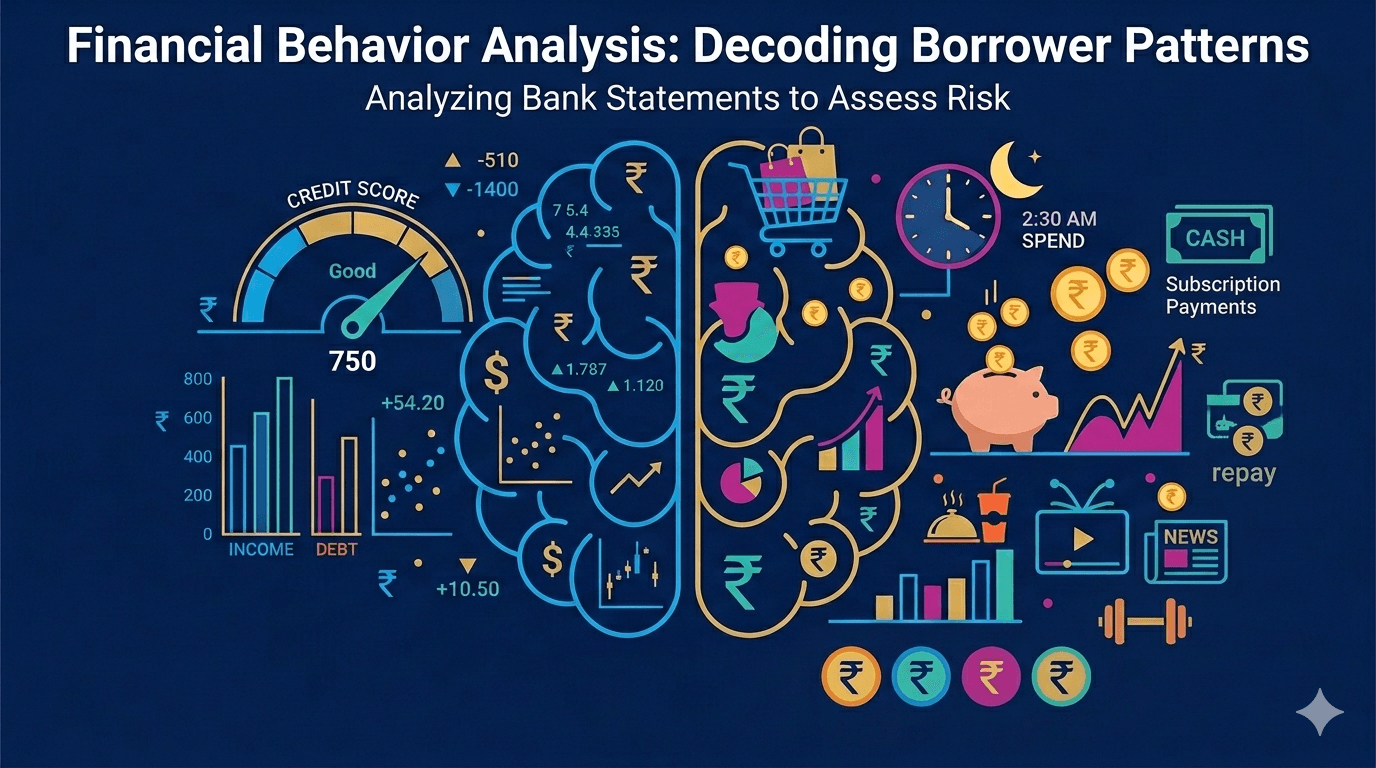

Behavioural Finance Patterns in Bank Statements: What They Reveal About Borrowers

In the traditional lending landscape, a borrower’s creditworthiness was often reduced to a single three-digit number: the credit score. However, for NBFCs and modern digital lenders, the “what” of a credit score is no longer sufficient without the “why” behind their spending. By leveraging deep-tier bank statement analysis, lenders can now move beyond static data

How to Scale to 1,000+ Daily Loan Applications Using Automated Bank Statement Processing

In the hyper-competitive fintech landscape of 2026, speed is the ultimate differentiator. Lenders are no longer just competing on interest rates; they are competing on Turnaround Time (TAT). However, scaling to handle thousands of applications often leads to a “hiring trap” the more you grow, the more manual credit officers you need. This is where